Iain Davis discusses this article with Jesse Zurawell here.

In Part 1, we looked at the many points of agreement that some of us in the West can find in the words of Vladimir Putin. We acknowledged the offer of a potential “multipolar world order” and recognised that the unipolar hegemony of the G7- and NATO-aligned “rules-based order” is often threatening, coercive and violent.

Yet, when we looked at the history of the ideas underpinning multipolarity, an uncomfortable realisation dawned. Those whom we might blame for the worst excesses of the unipolar world order have consistently supported and actively pursued the creation of the alleged multipolar alternative.

The multipolar world order advocated by Presidents Putin, Xi, Modi and others appears to stand in opposition to the current globalist order; yet there is evidence to suggest this may not be the case. For instance, the World Economic Forum’s so-called Great Reset promotes the same “regionalized” world.

What instead appears to be afoot, in both East and West, is a collective effort to redistribute global power. There seems to be a universal desire to exploit the disruption of supply chains, to “deglobalize”, and thereby to introduce true “global governance” in order to manage a geographical retreat while maintaining a shared global agenda on key issues, such as “sustainable development”.

Nowhere is this worldwide effort to change the balance of power more evident than in the global response to the conflict in Ukraine.

A Very Convenient War

The war in Ukraine is far from convenient for those suffering it. It is a part of an ongoing disaster, both for the people who live within Ukraine's current borders and those who reside in the new Russian republics and oblasts of Donetsk, Lugansk, Zaporozhye and Kherson. An end to the war can only be achieved through ceasefire and peace negotiations. Let's hope someone with sufficient influence can muster the will to start the process.

The Ukraine war has also accelerated the transfer of global power that began decades earlier and sped up during the pseudopandemic. The Western sanctions imposed upon Russia, in response to war, have predictably backfired disastrously. It almost seems as though their purpose is to degrade the global economy and Western economies in particular.

Energy flows have been redirected, and it is Eurasia and the Orient that is benefiting from comparatively cheap oil, gas and coal. The West is enforcing inflation-caused price austerity upon its population in order to pay, in the immediate and short term, for more expensive commodities, such as liquefied natural gas (LNG) from countries like Qatar and the US.

A clearer distinction between between European and American power is emerging. Old rivalries, supposedly long buried by the Anglo-American Establishment, have reemerged as European power casts an increasingly sceptical eye towards its American political and corporate partners.

This, in turn, is propelling an economic realignment that raises the distinct prospect of financial collapse. As noted by the World Bank, high inflation and low growth suggest that "the pain of stagflation could persist for several years".

In its 2022 Global Growth Prospects Report, the World Bank listed the numerous ways in which the sanctions and the Covid lockdowns have destroyed global economic activity. Yet, apparently in complete denial of everything it said within its own report, it bizarrely declared:

Russia’s invasion of Ukraine and its effects on commodity markets, supply chains, inflation, and financial conditions have steepened the slowdown in global growth.

Much like the pseudopandemic that immediately preceded it, Russia's war in Ukraine has actually not significantly impacted the global economy. The economic, financial, monetary and trade difficulties which the world now faces have been fuelled almost entirely by monetary and political decisions, primarily in the form of an unimaginable expansion of the money supply and the sanctions policy response to Russia's war in Ukraine.

Covid–19 didn't cause the precursor shut down of global supply chains either. Again, it was the selected policy response to Covid–19 that was responsible.

We really should ask what purpose these so-called global leaders are supposed to serve. Apparently, everything is beyond their control, their hands are tied, and they simply have to make the situation far worse than it would otherwise have been. Assuming they are not all idiots, we might wonder if there is not, in fact, some ulterior motive behind their policy decisions.

Growth in China has slowed but is still projected to achieve 4.3% for 2022 and 5.2% in 2023. The reduced rate of Chinese GDP growth is overwhelmingly due to China's "zero-Covid" lockdown policy folly. If we suspect the Western political class are an agreement-incapable lunatic fringe, hell-bent upon economic destruction and population control, there is no reason at all to believe the Chinese "princelings" aren't either.

It now appears that China's Covid policy regime may be softening slightly. As a result, global financial markets have seen an uptick. It seems an exquisite economic control system has been placed in the hands of President Xi’s administration. Domestic policy in China, not the US, now dictates global market fluctuations. As such, this represents a true global rebalancing of power.

Chinese and South-East Asian growth estimates stand in stark contrast to practically zero growth in Europe's hitherto powerhouse, Germany. It is a situation mirrored in the UK, France and elsewhere in Europe. Flagging economic activity in the US also continues, despite increasing American LNG and oil sales to China.

Meanwhile, in Russia—the supposed target of Western collective punishment—now that the country has weathered the initial impact of the sanctions, something nothing short of a reallocation of global trade, energy and financial flows is assisting national economic recovery.

The sanctions have also delivered some of Russia's and China's key long-term monetary policy objectives. They and other BRICS emerging economies (Brazil, India and South Africa) have been trying to "de-dollarize" their economies for more than a decade. The sanctions are delivering just what they have always wanted.

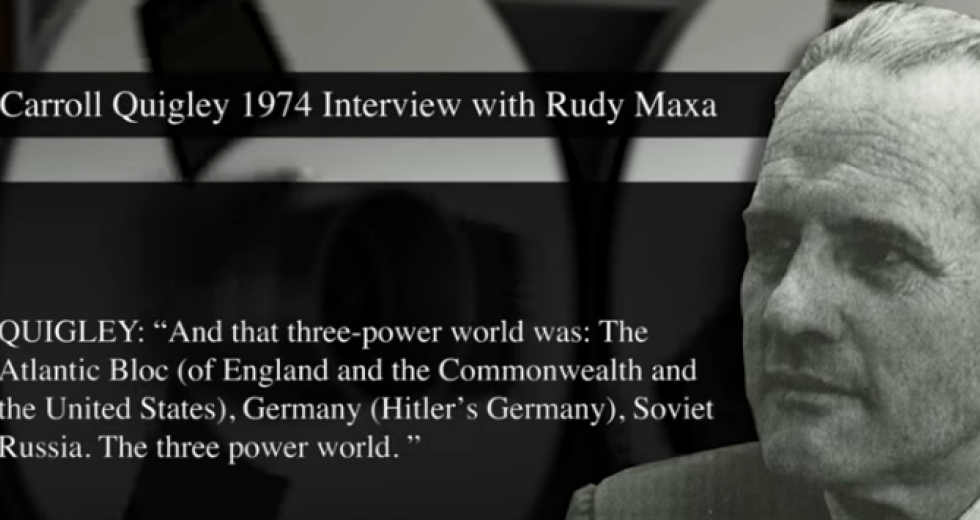

In return, it appears the the war has resurrected NATO from complete irrelevance. It has also reinvigorated the EU’s push toward military unification (designated as Permanent Structured Cooperation/PESCO). This raises the prospect of a “three-power world”—a tripolar geopolitics—with a balanced distribution of military power between the three continental blocs.

One of the "warnings" presciently given by Klaus Schwab and Thierry Malleret in The Great Reset was the potential collapse of the dollar as the primary global reserve currency:

Ultimately, the possible end of the US dollar’s primacy will depend on what happens in the US. As Henry Paulson, a former US Treasury Secretary, says: “US dollar prominence begins at home […] The United States must maintain an economy that inspires global credibility and confidence. Failure to do so will, over time, put the US dollar’s position in peril.”

Yet statements from the head of the Federal Reserve, Jerome Powell, who openly declared that "the US federal budget is on an unsustainable path", and others' comments, such as those of the US secretary of the treasury, Janet Yellen, have repeatedly cast doubt upon the credibility of the US economy and the dollar as a reserve currency. Yellen even resorted to arbitrarily raising the debt ceiling to avoid a US default on its debt obligations in 2021.

In the face of numerous, similar crisis in the past, the US financial oligarchy managed to cover them up with aplomb. For example, the scale of the Savings and Loans crisis in the US in the 1980s, which threatened a global economic and financial collapse, was almost completely hidden from the public.

While the mainstream media reported on it to a limited extent, the level of financial and economic risk that the world faced at that time was barely acknowledged. Most carried on blissfully unaware.

Now, however, not only have the leading voices of the US financial system suddenly opted for unusual candour, they have apparently done everything they can the make the current predicament worse. The sanctions against the Russian Federation quite obviously erode international trust in the United States as the issuer of a dependable reserve currency.

In The Great Reset, Schwab and Malleret noted how such incautious unilateral decisions would undermine the dollar:

US global credibility also depends on geopolitics and the appeal of its social model. The “exorbitant privilege” is intricately intertwined with global power, the perception of the US as a reliable partner and its role in the working of multilateral institutions. “If that role were seen as less sure and that security guarantee as less iron clad, [. . .] the security premium enjoyed by the US dollar could diminish” [quote attributed to Barry Eichengreen].

The US Administration presumably no longer wishes to enjoy its "exorbitant privilege". It appears determined to give a leg-up to a new global reserve currency system.

By seizing $630 billion of Russia's foreign currency reserves, it signalled to the rest of the world that its own dollar was no longer a stable reserve currency. Putin correctly observed that "everybody knows that financial reserves can simply be stolen".

This provided a massive American boost to Russian- and Chinese-led initiatives aimed at creating an alternative global reserve that benefits their economies—much as the dollar reserve system has benefited the US.

A Strangely-Fought War

As far back as April 2022—within weeks of Russia’s escalation of the Ukraine war that had in fact been ongoing for eight years—the then British Prime Minister, Boris Johnson, said that it was a “realistic possibility” that the war would last until the end of 2023.

Ukrainian mainstream media reported that Johnson subsequently made an impromptu visit to Kiev in May and pressured Ukraine's President Zelensky not to accept the framework for peace talks previously agreed by Ukrainian and Russian delegates in Istanbul. Apparently, the UK leader was not just foreseeing a lengthy conflict; he was doing all he could to ensure that a protracted war was a “realistic probability”.

The US-led NATO alliance has consistently fuelled the conflict with weaponry, but has not offered Ukraine the military support it would need potentially to secure victory. The NATO hierarchy has also cooled its enthusiasm to allow Ukraine to join the alliance—seemingly leaving the Ukrainian forces and people dangerously exposed, even literally.

At the same time, many Russia-based commentators are at a loss to understand the Kremlin’s approach to the “special military operation”. By launching a war without declaring a war, the Kremlin allowed NATO states to carry out their own “special military operations” in Ukraine. A “special military operation” is a term with no meaning in international law. Consequently, NATO states can contribute significantly to Ukraine’s defence without ever violating any third-party obligation of neutrality under international law.

Others ask why, if Ukraine’s air defences were destroyed in the first weeks of the conflict, Russia restricted its attack aircraft and strike helicopters to air support of front line troops only. Why didn’t Russia use its overwhelming air superiority to better effect?

Similarly, celebrity Russian mercenaries like Igor Vsevolodovich Girkin (alias Igor Ivanovich Strelkov) have asked why Ukrainian forces can use NATO-supplied HIMARS rocket systems to strike cities like Kherson and other key targets in the Donbas, without any significant air defence or response from Russian forces, most notably the Russian Air Force.

The much-vaunted Russian S–400 air defence system is neither designed nor particularly well suited to defend targets against the relatively inexpensive, short-range HIMARS. Nonetheless, the fact that the Russian Government is supplying its state-of-the-art weaponry to its supposed NATO opponents, while NATO is simultaneously supplying the weapons that Ukrainian forces use to kill Russian soldiers, only adds to the confusion of the picture.

Why did Russian forces proceed so slowly, thus allowing the Ukrainian Government and its allies ample opportunity to replenish Ukrainian losses? Why, after years of military personnel cuts while Russian forces were being streamlined and modernised, has Russia now engaged in a campaign so reliant upon troop numbers?

The present style of mass conventional warfare—based on sheer weight of numbers, like some throwback to the trenches of Verdun—has favoured the numerical advantage of the Ukrainian forces. Yet the Ukrainian Army, having retaken Kharkov and Kherson with apparent ease, then stopped and failed to progress to retake the key strategic objective of Zaporozhye. Why would the Russian military even engage in a large-deployment ground war, when its tactical military advantage is primarily technological? Why not exploit that technological and air-power superiority?

Time will perhaps reveal the answers to these perplexing questions. What can be said for now is that the unabating conflict has facilitated a remarkable financial and monetary transformation. This has largely resulted from the Western policy response to the Ukraine war. It is not unreasonable to speculate whether this is a possible rationale for maintaining hostilities regardless of the human cost.

Money Flowing East

In searching for a new global reserve currency, the WEF noted that China's renminbi (RMB; denominated internationally as the yuan, CNY) "could be an option, but not until strict capital controls are eliminated and the RMB turns into a market-determined currency". It seems that the Chinese Communist Party cadres have read The Great Reset too, because that is more or less what the Chinese Government has done.

In June 2021, China allowed additional capital outflows, thereby encouraging global investors, such as Goldman Sachs, to strengthen their ties with Chinese "partners". In March 2022—again, precipitated by the West's sanctions, as Russian energy, grain and other commodities increasingly flowed toward China—the People's Bank of China scrapped its restriction on cross-border capital movement.

Risking devaluation of the RMB became a secondary concern. In September 2022, China further relaxed foreign exchange restrictions. As reported by Bloomberg, China is pushing ahead with plans to internationalise its currency.

The recent move by China’s President Xi to increase the purchase of Saudi oil with the yuan on the Shanghai Petroleum and National Gas Exchange is yet another step closer to a potential petro-yuan, displacing the half-century-old petrodollar. China is Saudi Arabia’s biggest single trading partner; the Saudi Government has reportedly been considering the move for months. Some suggest this is brinkmanship by the Saudi régime to strengthen its negotiating position with the US, but that analysis overlooks the fact that China is now Riyadh's biggest market.

Yet again, in this case, it was the West's sanctions that helped the BRICS nations achieve a long-held monetary policy objective, In June 2022 the BRICS member states announced their plans to establish an alternative to the IMF's special drawing rights (SDRs). A basket of BRICS currencies will potentially form a new tradable asset to be exchanged for goods, services and commodities, or redeemed for equivalent currency value.

The sanctions imposed in response to Russia's war have also spurred on development in financial technology (FinTech). According to the NATO think tank, the Atlantic Council, 105 countries around the world—accounting for 95% of global GDP—are surging ahead with development of a central bank digital currency (CBDC).

Russia and China are among the leading developed nations in the race to establish CBDCs. The largest economy so far to have launched a national CBDC is Nigeria, but China, Russia, Kazakhstan and Ukraine are among the 15 countries to have also piloted theirs. The Atlantic Council notes that "the G7 economies, the US and UK are the furthest behind on CBDC development”.

The current British Prime Minister, Rishi Sunak, for his part, is likewise fully behind the Bank for International Settlements (BIS)-led efforts to develop a national CBDC. Admitting at the G7 conference that the UK was still in the exploratory phase, he exuded undiminished enthusiasm for programmable money nonetheless.

This sudden inability of Western powers to keep technological pace with the FinTech of emerging and developing markets seems strange because, in his 2019 address to G7 central bankers at the Jackson Hole symposium, then governor of the Bank of England, Mark Carney, said that there was an urgent need to build "multi-polar global economy" with a "new international monetary and financial system".

He suggested that a "Synthetic Hegemonic Currency [SHC] would be best provided by the public sector, perhaps through a network of central bank digital currencies". Carney added that the time had come to "build a system worthy of the diverse, multi-polar global economy that is emerging".

Sergey Glazyev, the former Russian Minister of Foreign Economic Relations and the current Commissioner for Integration and Macroeconomics within the Russian-led bloc, the Eurasian Economic Commission (the bureaucratic core of the Eurasian Economic Union), has been hailed as the "brilliant" mind behind the "emerging new multipolar financial architecture". Others have been equally effusive about Glazyev's "new global financial system" which has apparently leveraged "Moscow’s uber strategic portfolio".

In April 2022, Glazyev explained how the transition to the "multipolar financial structure"—which is the same "new international financial platform" referred to by Putin at Valdai—was progressing. Initially, according to Glazyev, countries would fall back on their own currencies and clearing mechanisms. He noted that, due to the sanctions imposed as a result of the Ukraine war, this "phase" was nearly complete.

The next phase, he said, was to establish new pricing mechanisms outside of the dollar. Again, thanks to the sanctions, that is precisely what is happening.

Trading in the yuan or a gold-backed currency showed promise, he said, but both had some technical and structural problems; neither could be a long-term solution. Thus Glazyev advocated his supposedly brilliant, "uber strategic" solution:

The third and the final stage on the new economic order transition will involve a creation of a new digital payment currency founded through an international agreement[.] [. . .] A currency like this can be issued by a pool of currency reserves of BRICS countries, which all interested countries will be able to join.

Glazyev was promoting a digital currency structured like the IMF's special drawing rights (SDR). This would be identical to a central bank digital currency (CBDC) tethered to a basket of currencies, like a stablecoin—a CBDC operating like a “synthetic hegemonic currency”.

As has been pointed out by German economic journalist and author Ernst Wolff, among others, it is a coincidence of almost incalculable improbability that, following the G7 bankers' emergency plea to create a new multipolar international monetary and financial system, global events in the space of just a couple of years—first the pseudopandemic and then the war in Ukraine—and more specifically the West's spending responses to these crises—should have coalesced so perfectly to move the world, with pinpoint precision, towards the specific monetary destination desired by the central bankers.

It seems that Glazyev's "brilliance" is that he knows how to deliver exactly what G7 central bankers want—largely thanks to the fact that the Western "unipolar world order" committed financial and monetary hara-kiri on the global stage in response to a war that the Russian Government escalated and that all parties have seemingly perpetuated.

Whatever else the Ukraine war may be, in terms of globalist ambitions for the international monetary and financial system, it is incredibly convenient. Doubtless, though, many will argue this is mere coincidence.

The Multipolar Bankers

This new international monetary and financial system, when it emerges, will be coordinated from Switzerland by the Bank for International Settlements. The BIS mission statement reads:

Our mission is to support central banks' pursuit of monetary and financial stability through international cooperation, and to act as a bank for central banks.

As the issuers of CBDCs, and as the institutions with control of national monetary, financial and increasingly fiscal policy, the national central banks will be coordinating their CBDC efforts—whatever form these may take—through the BIS.

All BRICS nations' central banks are currently listed as active participant member of the BIS. The BIS clarifies what this listing means:

Sixty-three central banks and monetary authorities are currently members of the BIS and have rights of voting and representation at General Meetings[.]

This clearly includes the Central Bank of the Russian Federation (CBR, alias Bank of Russia)—despite the fact that the BIS has ostensibly ostracised the CBR.

There has been no official statement from either the BIS or the CBR on this matter. We only have mainstream media reports, citing a single statement from an anonymous BIS spokesperson, and some ambiguous footnotes on a couple of BIS documents, to attest to this alleged suspension.

BIS Paper 123—published in late April 2022, after the alleged Russian suspension—explores and endorses the CBR’s relatively advanced progress with its “digital rouble” (CBDC).

It states in a footnote:

The access of the Central Bank of the Russian Federation to all BIS services, meetings and other BIS activities has been suspended.

The determiner all in collocation with a negative statement (of which the above is rhetorically a loose kind) is a distinctly ambiguous construction in English, the more so given that German usage may have influenced the above BIS wording in English. Does the above footnote mean that the CBR enjoys no access to any BIS services? Or does it mean that it can no longer access the whole gamut of BIS services but has retained access to some? If so, which ones?

Why is the CBR currently listed by the BIS as an active participant central bank with full voting rights at Basel? Why is the US House of Representatives Committee on Armed Services currently trying to exclude the CBR from the BIS if it is already suspended?

In the annual allocation of the CBR governor's duties, published on 19 December 2022, it is the current duty of the Russian central bank head to ensure:

[...] participation of the Bank of Russia in the G20, the International Monetary Fund, the Financial Stability Board, the World Bank, the Bank for International Settlements and the Financial Sector Assessment Program (FSAP)[.]

The evidence that the CBR has actually been suspended from the BIS is thin. The claims of the Western mainstream media to that effect should, during the propaganda of war, be treated with caution.

As discussed in Part 1 of this article, the multipolar world order is a variation of the three-power world, as first envisaged by the Rhodes-Milner group and as subsequently recast by the Rockefellers and later enhanced by the World Economic Forum. The practical political embodiment of this new world order already exists, in the form of the G20.

Russian and Chinese governments attached to Western banking

The G20, created in 1999 by G7 central bankers—in response a global crisis, of course—organises nation states into five groups. Groups 1 and 2 are formed broadly around shared policy objectives, with Groups 3 to 5 aligned more by geographical region. You could call these latter groups "three poles", if you like.

In their joint statement on global sustainable development in February 2022, Putin and Xi were eager to highlight a growing role for the G20. They put the G7 central bankers’ model at the heart of the multipolar system of global governance:

The sides [signatories] support the G20 format as an important forum for discussing international economic cooperation issues and anti-crisis response measures, jointly promote the invigorated spirit of solidarity and cooperation within the G20, support the leading role of the association in such areas as the international fight against epidemics, world economic recovery, inclusive sustainable development, improving the global economic governance system in a fair and rational manner to collectively address global challenges.

In order for global governance and the new—multipolar—international monetary and financial system to have real teeth, a centrally coordinated global tax system will be necessary. This will usher in global taxation without representation and the complete eradication of any notion of national sovereignty.

In December 2021, with the full support of the Russian and Chinese governments, alongside their BRICS partners, the G20 and the Organisation for Economic Cooperation and Development (OECD) issued the world's first firm declaration to establish a global tax régime. This was the official launch of a plan first hatched in St Petersburg, Russia, more than a decade earlier.

Allegedly, the “Two-Pillar Solution to Address Tax Challenges” will tackle the tax avoidance schemes employed by “multinational enterprises”. We can safely anticipate that multibillion-dollar corporations will employ the most expensive tax lawyers in the world, who will make mincemeat of any such agreement before the ink is dry.

So the point is not actually to put paid to corporate tax evasion; that is a sales pitch for the gullible. The purpose of this "solution" is to establish the framework for a centrally controlled, global tax system.

In 2020, Jack Ma, the multi-billionaire founder of and executive chairman of Alibaba Group, gave an address at the Bund Finance Summit in Shanghai. Among the attendees listening to Ma was Lord Jim O'Neill, representing the London-based policy think tank, the Royal Institute for International Affairs (Chatham House).

In 2001, it was O'Neill—then as chairman of the bulge bracket investment firm Goldman Sachs—who first introduced the world to the concept of the BRIC emerging markets (South Africa, the final capital S of the acronym, had not yet joined the bloc). He somehow managed to predict that their GDP growth would one day outstrip that of the G7. The West's bulge bracket subsequently made the strategic foreign direct investments that ensured that it now does outstrip the G7.

Jim was in good company in Shanghai. He was joined by, among others, Robert Rubin (Council on Foreign Relations), Jean-Claude Trichet (Trilateral Commission), Alderman William Russell (Corporation of the City of London), Zhang Tao (International Monetary Fund), Yi Gang (People's Bank of China), Tony Blair (Institute for Global Change) and Benoît Cœuré (Bank for International Settlements).

At the time of Ma's since-notorious talk, his Ant Group—an Alibaba affiliate—was poised to launch the biggest initial public offering (IPO) in stock exchange history. Investors across the world were salivating at the prospect. Unfortunately for Ma and eager investors, prior to the IPO he delivered his controversial Bund speech. He then disappeared from the face of the earth for three months, and the Chinese regulatory authorities cancelled the IPO, wiping nearly $76 billion off Ant Group's value overnight.

The Western mainstream media lied about the content of that speech. They focused disingenuously upon Ma’s relatively minor criticism that Chinese commercial banks operated with a "pawnshop mentality". Western media falsely framed Ma's critique as an attack on Xi Jinping's proposed banking reforms.

While Ma did criticise the Chinese financial industry, his comment with regard to President Xi’s proposed reforms was this:

[W]hat President Xi said about “enhancing governing ability” means to maintain healthy and sustainable development under orderly regulation, not no development due to regulation.

The bulk of Ma's criticism was reserved not for Chinese financial regulators but rather for the most powerful bank in the world, the Bank for International Settlements. The Western mainstream media didn't even mention this in any of its misleading propaganda reports of Ma’s speech. Indeed, the Western mainstream media rarely care to mention the BIS at all.

In response to the 2008 financial crash, the BIS rolled out the third in a series of Basel Accords, intended to reduce commercial banks', and the wider financial industry's, risk exposure. It was these liquidity ukases imposed upon the world from Basel that Ma was attacking, along with those behind the “international rules-based order” and its international monetary and financial system:

[T]he Basel Accords talked about risk control, which has been gaining more and more attention, to the point that it became an operational standard for risk control. [. . .] This, in fact, is the root cause of many of the world's problems today. [. . .] Basel, more like a seniors club [comment by Iain Davis: a direct reference to the BIS itself], is about solving the problem of an ageing financial system that has been operating for decades. [. . .]

The Basel Accords [are] designed to treat the diseases of the elderly with an ageing system and over-complexity[.] [. . .] To make risk-free innovation is to stifle innovation, and there is no risk-free innovation in this world. [. . .] Many regulatory authorities around the world have become zero risk, their own departments have become zero risk. [. . .] Collateralization with a pawnshop mentality is not going to support the financial needs of the world's development over the next 30 years.

The Chinese authorities certainly acted swiftly, and Ma at the very least had to lie low. It seems it was Ma’s criticism of the BIS and the "seniors club" of globalist financiers with their "ageing system" that incurred the wrath of China's technocratic government. They silenced him and punished his business accordingly.

They didn't do so because they are aligned with the unipolar "international rules-based order" or the oligarchs who control it. They did so because they have an existing partnership with the global financial class—the same class that has been the supporting hand behind China’s technological and economic development for decades.

So who does want a multipolar world order?

In 2018 the founder and Executive Chairman of the WEF, Klaus Schwab, wrote about what he called Globalization 4.0. Referring to the Western consensus on the "international rules-based order", he said:

After World War II, the international community came together to build a shared future. Now, it must do so again. [. . .] Globalism is an ideology that prioritizes the neoliberal global order over national interests. Nobody can deny that we are living in a globalized world. But whether all of our policies should be “globalist” is highly debatable. [. . .]

[T]his moment of crisis [comment by Iain Davis: the slow economic recovery after the 2008 crash] has raised important questions about our global-governance architecture. [. . .] Moreover, the challenges associated with the Fourth Industrial Revolution (4IR) are coinciding with [. . .] the advent of an increasingly multipolar international order[.] [. . .] These integrated developments are ushering in a new era of globalization.

The WEF expanded on this “new era of globalization” in the accompanying white paper:

[T]he post-war governance architecture of Globalization 2.0 and 3.0 was mainly designed to mediate national interests through formal norms negotiated by states, the enabling architecture of Globalization 4.0 must marshal a much wider geometry of actors and governance arrangements[.]. [. . . ]

One of the benefits of this more multidimensional and agile conception of global cooperation is that it expands the range of opportunities for states and other actors to locate their common interests and give them practical expression in our increasingly multipolar and multiconceptual world. Such calibrated, consensual steps can help to build the trust necessary to expand the ambition of collective action and multilateral norms in subsequent stages.

Just as do the international bankers and financiers, the WEF’s wider corporate network supports the creation of the multipolar world order. The pseudopandemic and the war in Ukraine have been the “subsequent stages” that have calibrated the “consensual steps” to enable the expansion of the WEF’s "range of opportunities". This will assist the entire global ruling class, including and extending beyond the WEF, to achieve their "ambition of collective action". Multipolarity is the essence of "Globalization 4.0".

The open "transformation" of global governance to the multipolar system is simply the public disclosure of that which was already extant. The New World Order has been repackaged as "multipolar" and is now being advocated as some kind of escape hatch from itself.

On 30 September 2022, President Putin issued Decree No. 693 "on the definition of an organisation that ensures the development of a digital technologies for identification and authentication". It establishes the Centre for Biometric Technologies Joint Stock Company (CBT JSC). The Russian Government will own 26% of the stock directly, the central bank 25%, and the state-owned telecommunications corporation, Rostelecom, will own 49%.

The Central Bank of Russia (CBR) is entirely independent of the Government of the Russian Federation. This, combined with the the other ownership structures within the JSC, means that “the state will not have a controlling stake in this JSC”. Russian’s most personal data will be controlled by a public-private partnership.

On 13 October 2022, Kommersant reported that "the Moscow data storage centre will collate video streams from the country’s cameras". The Kremlin-sceptical business paper added:

The Moscow Department of Information Technologies plans to finalise a unified data storage centre, at whose facilities the capital's facial recognition system operates, to centralise the collection of video streams from all regions of the country. [. . .] Centralising the analysis of video information is becoming pertinent due to the heightened terrorist threat and the hunt for draft-dodgers.

As Russian citizens are hurled deeper into the Fourth Industrial Revolution, the World Bank has praised—not criticised—Russia as a world leader in terms of its ability to exert technological and information control over the lives of its citizens. The Russian surveillance state that is emerging is truly horrifying. In November 2021, in an innocuous-sounding decree on transport strategy, amid plans for the 3D printing of food stuffs, the Kremlin stated:

The introduction of neural interface implants will lead to the transfer of functions from smartphones into implants[.] [This] will allow for the possibility of unambiguous identification of passengers and operating personnel, [and] integration systems of geopositioning with implants for the creation of personalised transport products.

Both the Russian and the Chinese governments were signatories to the G20 Bali Leaders' Declaration. As such, they signalled their unwavering support for:

- Agenda 2030

- “sustainable development”

- stakeholder capitalism

- public-private partnerships and “innovative financing”

- the Fourth Industrial Revolution

- censorship

- information governance

- a global pandemic treaty

- the integration of vaccine certificates into a single global digital ID

- the roll-out of CBDCs

- the restructuring of the international monetary and financial system

- the creation of new markets for vaccines

- and the global governance of every aspect of our lives.

There was not a squeak from the BRICS’ national “leaders”, those strongmen who supposedly stand against the tyranny of the unipolar “rules-based” system. There was no disagreement between national governments allegedly opposed to each other in propaganda and on the battlefield. The agenda is global, and the multipolar world order isn’t going to save anybody from it.

Conclusion

At some point, as global governance becomes an imminent reality, then we, the people, will have to be invited or coerced to buy into it. We can mount overwhelming resistance and end the ambitions of the globalists if we choose to act collectively. This being so, the conditions are going to have to be created to cajole us to accept, or perhaps even welcome, the imposition of genuine centralised global authority.

Consequently, we have been given new heroes and new centres of power to believe in. Putin and Xi are held up as leading the fight against the evil machinations of the unipolar despots. The resultant propaganda appears to be bearing fruit.

Putin’s appeal to disaffected Westerners in his Valdai speech couldn’t have been more enticing. He encapsulated the argument of millions, presenting exactly the kind of “opposition” they want to see. Meanwhile, the Russian state he represents is a world leader in the deployment of the tools of global technocratic control.

We are finally being openly invited to accept totalitarian global governance based upon the deceit that it is the only way to stop the other form of totalitarian global governance that we reject. Perhaps if we place our faith in yet another set of great leaders, things really will get better this time.

Sadly, until we grasp that fact that the political systems which we still abide—no matter where we live on this planet—are designed to oppress and control us, we are likely to remain expendable pawns in perpetuity. To beseech the political class for remedy, while their power stems from the systems that are oppressing us, is slave mentality.

As Professor Mark Crispin Miller recently highlighted, perhaps in searching for hope, even the very best of us are potentially overlooking the malignancy of multipolarity, seeing enmity where it doesn't exist and ignoring complicity where it does.

This does not mean that Putin, Sunak, Schwab, Xi, Modi, Biden and other “global leaders” all agree on how the multipolar world order should be constructed; they simply agree that its time has come. The public disagreements and confrontations are often indicative of real squabbles, rather like the back-stabbing you might find in any boardroom.

They each have their sets of oligarchs behind them, and the oligarchic clans each want to maximise their own influence in the new global order. But, as can be seen from their statements and policy initiatives, all agree upon the framework of multipolarity, replete with its insidious technocratic control systems. They may bicker, but they all want the corporation to prosper, because it is the source of their fraction of global power, whether that fraction waxes or wanes.

If we consider, for example, the WEF’s Great Reset, what are our deepest concerns about the emerging global order it advocates? Is it not the global surveillance state? Have we ceased our opposition to the total enslavement that CBDCs will bring? Do we no longer wish to resist the imposition of social credit, the digital ID control grid, artificial GM food products, genetic modification tinkering with nucleosides, the biosecurity state and transhumanism?

If we still wish to oppose these oppressive control mechanisms, then why would we ever contemplate accepting, or even hope for, a multipolar world order? Is this not a global governance system led, as we have seen above, by the governments and political leaders that are furthest advanced in the actual, real-world installation of the technological panopticon?

The governments around the world that openly declare their support for the multipolar world order are no worse than their G7- and NATO-aligned counterparts. But the West also seeks multipolarity, if surreptitiously.

The proposed multipolar world order is neither new nor any kind of salvation. We should reject it—just as we should all ongoing attempts to subjugate humanity under the deceptive guise of global governance.