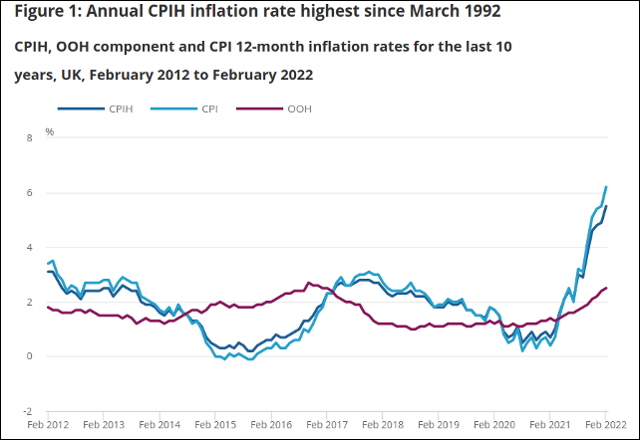

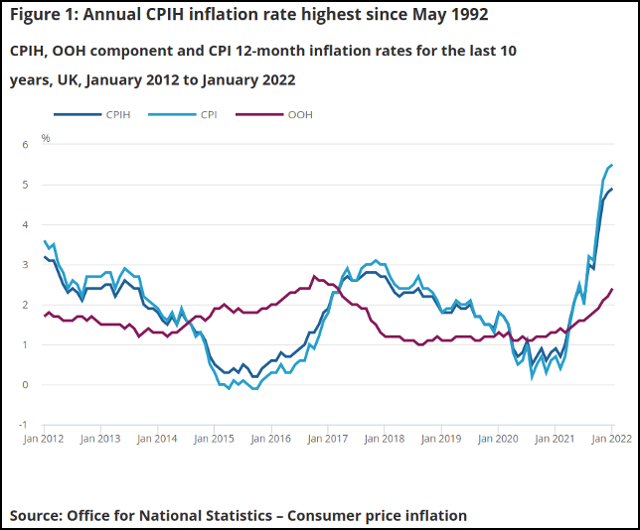

According to the UK Government, inflation is soaring and there is little they can do about it due to Russia’s military operation in Ukraine. However, a very basic check of the Office of National Statistics’ monthly inflation report clearly shows that price inflation was rapidly escalating long before the Ukrainian crisis began.

The average consumer price inflation figure, over the last ten years, had varied between 0% and 3%, with an approximate mean average of around 2%. By October 2021, it had hit the 4% mark, climbing quickly to around 6% by February 2022. Russia’s intervention in Ukraine, and the global sanctions that have followed, will exacerbate the situation, but it is unrelated to the cause of that inflation.

You could be forgiven for imagining that inflation is simply a natural consequence of the ebb and flow of normal, everyday economic activity. You would certainly be left with that impression if you read the BBC article What is the UK’s inflation rate and why is the cost of living going up?

The BBC informs us that inflation is calculated using the Consumer Prices Index (CPI). This measure is inadequate, although the BBC doesn’t bother to mention that. As we shall see, the CPI is only partly analogous to the real impact of inflation. A slightly better measure is the CPIH, which includes housing costs; but even this fails to provide the full picture.

The BBC says that the current rise in inflation—which is already the highest it has been for thirty years—is caused by the increase in energy prices. This has a knock-on cost for the production and delivery of all goods and services, not to mention higher domestic energy bills. The BBC adds that Brexit and an alleged pandemic added further inflationary pressure.

The BBC claims that these combined factors have necessitated higher wages and notes that, in such conditions, an additional 1.25% hike in National Insurance (the separate British tax granting eligibility for state welfare) increases the financial strain felt by employers.

The above is a reasonable report of the official inflation narrative.

Most of us understand that the economy is a highly complex system of human interactions, trade and exchange, driving supply and demand. When supply outstrips demand, prices fall; when demand is greater than supply, they rise. Higher energy prices, changing trade relations and natural disasters are bound to impact inflation and the economy.

The BBC reaffirms this understanding but, by omission, its piece is misleading. The underlying assumption the BBC asks us to accept is that our financial and political leaders do little to influence economic inputs.

Essentially, the BBC is claiming that inflation is a quasi-organic reaction to global forces beyond anyone’s control. This is the official myth of inflation.

Hiding Real Inflation

Inflation is actually a monetary and economic policy decision. It is a deliberate stealth tax and a tool for the transfers wealth from the people to the bankers and other globalists.

The post-Second World War progressive Western economic model was largely founded upon the ideas of the economist John Maynard Keynes (Baron Keynes of Tilton). In his 1920 publication The Economic Consequences of Peace, Keynes wrote:

Lenin is said to have declared that the best way to destroy the Capitalist System was to debauch the currency. By a continuing process of inflation, governments can confiscate, secretly and unobserved, an important part of the wealth of their citizens. By this method they not only confiscate, but they confiscate arbitrarily; and, while the process impoverishes many, it actually enriches some. […] Those to whom the system brings windfalls, beyond their deserts and even beyond their expectations or desires, become "profiteers." […]

Lenin was certainly right. There is no subtler, no surer means of overturning the existing basis of society than to debauch the currency. The process engages all the hidden forces of economic law on the side of destruction, and does it in a manner which not one man in a million is able to diagnose.

Keynes was a eugenicist, serving as treasurer of the Cambridge University Eugenics Society, chairman of the Malthusian League and vice-president of the British Eugenics Society. Shortly before his death, in 1946, he opined that eugenics was “the most important, significant and, I would add, genuine branch of sociology.”

As an avowed advocate of eugenics—the scientific basis for which is risible—Keynes believed in the notion of hereditary genius suggested by the patron of social Darwinism, Francis Galton. Keynes, like Galton, was among that ruling class which considered it their right to command society by virtue of their superior breeding. As such, he greatly underestimated our ability to correctly diagnose the “hidden forces of economic law”.

The problem is not that we are too stupid to understand these forces; it is that they remain largely hidden from public scrutiny. We only need to read anonymous BBC opinion pieces on inflation to understand that this concealment continues today.

The official inflation myth is that it is caused either by increasing production costs (cost-push) or rising demand (demand-pull). These are not the causes of inflation; they are a consequence of inflation.

Inflation presents the producer, the service provider or the investor with potential risk. If the consumer can no longer afford the higher prices, it could quickly become uneconomical to do business. Inflation is a game of winners and losers.

If you stack the cards in your favour, you can be a winner. The consumer is always the loser, mostly because we aren’t even in the game. We are practically non-playing characters—and we all know what happens to them. We are also the cash cows whom Keynes’ profiteers farm.

It is acknowledged that demand-pull, in particular, can provide an opportunity for producers and service providers to boost profits by ratcheting up their prices. Cost-push can also enrich investors: if they hold assets in companies whose prices rise faster than underlying—though growing—costs, or if they are invested in commodities that are increasing in price. As the subsequent stock price goes up, the savvy investor who trades at the top of the market can make a killing.

However, this is not the “profiteering” that Keynes was referring to. For some, inflation always brings windfalls, and, throughout history, such players have exploited inflation, often deliberately causing it, to appropriate more wealth and influence for themselves. They do so knowing that it will throw large swathes of the population into penury. They don’t care.

As Alexander Dielius, the then CEO of Goldman Sachs in Germany, said in 2010:

Fairy DustBanks do not have an obligation to promote the public good.

Money is created out of thin air: predominantly by private commercial banks, but also by the private central banks. It is conjured using a spell that we can call debt monetisation.

Professor Richard A. Werner demonstrated that commercial banks create money at will. In his paper Can Banks Individually Create Money Out Of Nothing?, he reported how he had gained direct access to a commercial bank’s balance sheet. Next, he took out a €200,000 loan, in order to monitor the bank’s assets and liability changes.

Prof. Werner observed:

The bank did not transfer the money away from other internal or external accounts […] it was found that the bank newly ‘invented’ the funds by crediting the borrower's account with a deposit, although no such deposit had taken place. This is in line with the claims of the credit creation theory.

The commercial bank recorded the loan agreement as an asset and then credited an equivalent amount, calling it a deposit, into Prof. Werner’s account. From nothing, other than Werner’s signature, they created new purchasing power that did not previously exist. They had converted a debt into new money: debt monetisation.

For more than a century, economists and bankers have bamboozled the public with seemingly ever more complex explanations about how money is created. This is part of the monetary dissimulation that the establishment has long maintained. Werner’s paper ends the reach of this duplicity, for anyone who reads it.

There is no doubt that some within the financial hierarchy have always known that money is created as what Werner termed “fairy dust”. Speaking in 1924, less than four years after Keynes wrote the Economic Consequences of Peace, then Chairman of the Midland Bank, Reginald McKenna, the former First Lord of the Admiralty, Home Secretary and UK Chancellor of the Exchequer (finance minister), said:

I am afraid the ordinary citizen will not like to be told that the banks or the Bank of England can create or destroy money. We are in the habit of thinking of money as wealth, as indeed it is in the hands of the individual who owns it, wealth in the most liquid form, and we do not like to hear that some private institution can create it at pleasure. It conjures up a picture of an autocratic and irresponsible body which by some black art of its own contriving can increase or diminish wealth, and presumably make a great deal of profit in the process. But I need hardly say nothing of the sort happens.

McKenna knew this a century ago. His equivocation was probably added to reassure his audience that he wasn’t about to let the cat out of the bag. In 2014, the Bank of England admitted the same:

Whenever a bank makes a loan, it simultaneously creates a matching deposit in the borrower’s bank account, thereby creating new money.

Even the so-called mainstream media acknowledge the truth. Yet still some would have you believe that this isn’t so. Writing for Forbes in 2015, former banker and financial systems designer Frances Coppola wrote:

[I]t is entirely incorrect to say that money is ‘spirited from thin air.’ It is not. […] Nor does the creation of money by commercial banks through lending require any faith other than in the borrower’s ability to repay the loan with interest when it is due. Mortgage lending does not require ever-rising house prices: stable house prices alone are sufficient to protect the bank from loan defaults. […] There is no ‘magic money tree’ in commercial banking.

Coppola is a banking expert and suggests that the balance between assets (loan contract) and the bank’s liabilities (so-called deposits) impacts the banks equity (calcualted as assets minus liabilities), thereby restricting how much they can lend. She does not appear to understand that, in both cases, the money for the loan or mortgage did not physically exist prior to completion of the contract (loan agreement).

The bank (lender) did not have this money anywhere on its balance sheet: neither as an asset nor a liability. The deposit wasn’t a movement of capital, it was the creation of capital.

Contrary to Coppola’s insistence, the commercial banks really do magic money out of thin air. When they subsequently earn interest on the “capital loan”, this becomes their asset. They acquired it by doing nothing. This then shores up their equity; and, over time, by repeating the same magic trick ad infinitum, banks create equity (liquidity) from fairy dust.

However, Coppola did identify the problem when central banks create money this way:

A central bank can create money without limit, though doing so risks inflation. […] If the central bank creates more money than the present and future productive capacity of the economy can absorb, the result is inflation.

Governments borrow by trading government bonds, known in the UK as gilt-edged securities or simply gilts. A government bond is a debt security issued by a government. They are generally considered low-risk investments, as they are backed by the state. This means they are funded by you and me: the taxpayer is on the hook for the inflation scam.

Just as commercial banks create money from nothing when they loan money to a private individuals or businesses, the process is practically identical when central banks purchase gilts and lend money to the government. It is the same creation of fairy dust.

Unfortunately, this is fairy dust that the taxpaying public has to repay, mostly by selling our labour. Government borrowing and subsequent taxation not only makes debt slaves of us, it enslaves future generations to the same profiteers.

Push, Pull and Expansion

A rise in supply costs (push) and escalating demand (pull) are factors that can emerge largely as a consequence of inflation, which is a condition of continuous price increases. These can then compound inflation but they did not cause it. The Bank of England (BoE) states:

Monetary policy is action that a country's central bank or government can take to influence how much money is in the economy and how much it costs to borrow. […] We set monetary policy […] Low and stable inflation is good for the UK’s economy and it is our main monetary policy aim.

The BoE suggests that inflation is “good” and indeed that it is the primary objective of its monetary policy. It defines inflation as “a measure of how much the prices of goods and services have gone up over time”. This CPI measure suggests that inflation is an inevitable consequence of normal “free market” economic activity driven solely by supply and demand (push and pull).

Yet the BoE admits that its own monetary policy controls inflation: “Monetary policy affects how much prices are rising — called the rate of inflation.”

Inflation is not independent of money creation, which is the monetisation of debt. The BoE also acknowledges that we do not live in a free market economy.

Market regulation alone testifies to this fact. Push and pull exacerbates inflation but, as stated by the BoE, it is the central bank’s monetary policies that cause it. Both market regulation by the state and monetary policy are mechanisms entirely alien to free markets.

While is true that a basic tenet of free market economics is price-setting in response to supply and demand, for inflation to dominate market conditions (as it always does), you need an expanding money supply and amenable government policy. Government policy, such as shutting down supply chains in response to an alleged global pandemic, interferes with and frequently destroys economic activity.

Monetary expansion (more of it) decreases the relative unit value of money by increasing the “money supply”. Consequently, a better way to think of inflation is a reduction in the purchasing power of money.

Throughout the pseudopandemic, we have become accustomed to changing definitions. The definition of words like “vaccine” and “immunity” have been changed to suit the policy agenda. This is nothing new.

The word “inflation” used to mean expansion or swelling (this being the original etymology of inflation) of the money supply. Today, with the assistance of propagandists like the BBC, that true meaning has been obscurred. Speaking in 1951, the economist Ludwig von Mises said:

Inflation, as this term was always used everywhere and especially in this country [the United States], means increasing the quantity of money and bank notes in circulation and the quantity of bank deposits subject to check. But people today use the term “inflation” to refer to the phenomenon that is an inevitable consequence of inflation, that is the tendency of all prices and wage rates to rise. The result of this deplorable confusion is that there is no term left to signify the cause of this rise in prices and wages.

There is no longer any word available to signify the phenomenon that has been, up to now, called inflation. It follows that nobody cares about inflation in the traditional sense of the term. As you cannot talk about something that has no name, you cannot fight it. Those who pretend to fight inflation are in fact only fighting what is the inevitable consequence of inflation, rising prices. Their ventures are doomed to failure because they do not attack the root of the evil.

The BoE offers a tool to see how the value of money has declined. In 1970, £10 would have purchased goods or services which, in 2021, would have been valued at £363.61. Another way of saying this is that the pound has devalued by more than 97% in just over 50 years.

The BoE claims its annual inflation target is 2%, yet the underlying rate that actually led over that half-century to the 97% devaluation of our currency is 5.2%. One has to wonder what useful purpose the Old Lady of Threadneedle Street serves.

Conversely, it is not difficult understand why the BoE claims inflation is “good”—though it is worth remembering that John Maynard Keynes called it the surest means of “overturning the existing basis of society”.

Inflation Profiteering

The economist Milton Friedman said:

Inflation is always and everywhere a monetary phenomenon in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output.

By “output”, Friedman meant the fruits of the productive economy, usually measured using the calculation of gross domestic product (GDP). It can be defined as:

The total monetary or market value of all the finished goods and services produced within a country’s borders in a specific time period.

When the creation of fairy dust vastly outstrips real-world GDP, then the excess of money circulating in the economy can—as Friedman highlighted—only result in inflation. Throughout history, whenever this situation has reached an extreme, hyperinflation (a monthly inflation rate above 50%) has frequently been the result.

The US Civil War, the collapse of the Weimar Republic in Germany in the 1930s and the more recent political turmoil in Zimbabwe have all seen governments rely upon monetary expansion to supposedly deal with the crisis. All this can achieve is rampant inflation which always makes the situation worse for ordinary people. However, for some it is a windfall.

Exploiting inflation for personal gain begins with expansion of the money supply but, in order to profit from it, the Cantillion Effect is milked. The eighteenth-century economist Richard Cantillion recognised that money creation benefits those who are first able access the new money supply.

New money is not distributed evenly. The earliest recipients have an advantage over those who have to wait for it to trickle down through the economy. With each investor taking a profitable cut along the way, by the time it has trickled down to the lower paid, there isn’t much left.

Let's assume the Bank of England creates £1,000 in new money. At the starting point of this fiat, monetary expansion has yet to cause any inflation. So, at the prices that obtained before this money creation, those who first access this money can purchase (invest) a full new £1,000 worth of assets, goods and services. For example, they could purchase £1,000 worth of natural gas futures on the New York Mercantile Exchange (NYMEX).

As the money supply expands, however, inflation kicks in, push and pull factors are skewed and asset and commodity prices start to rise. Due to inflation, the next group who access £1,000 of the new money may only be able to buy the pre-inflation equivalent of £900 worth of assets, goods or services.

By the time working people get the new money in their wage packets, a £1,000 fillip may only buy a relative amount of £750 worth of goods and services. Meanwhile, the first recipients have seen the value of their original asset increase to £1,250, as a result of inflation.

In reality, the relative gains and losses are measured in mere fractions of percentage points, not by the large margins used in our example. However, due to the scale of the world’s economy, this facilitates a Cantillion effect that is measured globally in trillions (millions of millions).

The early recipients of new money are relatively few and trade in hundreds of millions, often billions of new pounds, yuan, euros or dollars. By the time this new money trickles down to us, the effect is diluted severely; we number in the billions and are buying goods and services typically valued in mere tens of national currency units.

The is the rudimentary basis for the inflation profiteering that Keynes was referring to. However, as Keynes probably well knew, these windfalls are not beyond the well-informed expectations of some profiteers.

A select few have the financial power to create the conditions for inflation. Knowing that their actions will cause price increases, they can position themselves, not only to profit financially from inflation, but also to use it to consolidate their authority over the economy.

The question, then, is who gets the new money first, because they are the inflation profiteers. The answer to this is the obvious one: the banks, especially the central banks.

The Nitty-Gritty of Inflation Profiteering

In December 2021, the British House of Lords released its report into the UK Government’s Public Spending During the Covid-19 Pandemic. The total costs of the response measures was estimated to be between £315 billion and £410 billion, which equates to about £4,700 to £6,100 for every person in the UK.

To pay for this, the government borrowed on an unimaginable scale. In financial year 2019/20, the borrowing target for 2020/21 was £55 billion. In response to the pseudopandemic, however, the state borrowed £323 billion. The British response—including vaccine development support, furlough (keeping sent-home workers on pay) schemes, business support packages and additional NHS funding—was overwhelmingly, if not entirely, funded by government borrowing.

The Lords’ accompanying report, also published in December 2021, Coronavirus: Economic Impact, highlighted the other crushing effect of the pseudopandemic response on the economy. They noted:

The magnitude of the recession caused by the pandemic is unprecedented in modern times. GDP declined by 9.7% in 2020, the steepest drop since consistent records began in 1948 and equal to the decline in 1921. […] Government debt […] has inevitably increased. Going into the pandemic, government debt was equivalent to around 80% of GDP, it is 95% of GDP.

Of course, it wasn’t a low-mortality repiratory disease that “caused” the economic collapse. It was government policy.

As many warned, including the UK Column, the hardship hardwired into that policy response would obviously have a more devastating impact on the nation, including its public health, than COVID-19 could ever have had.

Not only did their Lordships avoid any mention of this fact; they also appeared to provide an overly optimistic assessment of the size of the national debt as a percentage of GDP. According to the Office for National Statistics (ONS), by March 2021 the national debt already represented 103.7% of GDP.

When the BoE monetises state (taxpayer) debt on this scale, it has to give it a technical-sounding name to avoid frightening us. So-called Quantitative Easing (QE) is supposedly a helpful term. The BoE is very patent about the fact that QE debt monetisation is the manufacturing of fairy dust:

Quantitative easing involves us creating digital money [.] to buy things like government debt in the form of bonds […] By creating this ‘new’ money, we aim to boost spending and investment in the economy.

On 19 March 2020—the same day that Public Health England (now the “UK Health Security Agency”) downgraded COVID-19 from a High-Consequence Infectious Disease (HCID) due to its low mortality rate—the BoE gave notice of its Asset Purchase Facility (APF) to “tackle the spread of Covid-19”. In addition to monetising government debt (by buying gilts), the BoE thus entered the secondary bond market. This “market operation” enabled the central bankers both to repurchase traded government bonds and to buy corporate bonds.

Just like the government, private corporations can issue bonds (a security) to raise capital. As with government bonds, these are issued on the primary market but overwhelmingly traded on the secondary market. The APF enabled the BoE to step up debt monetisation even further.

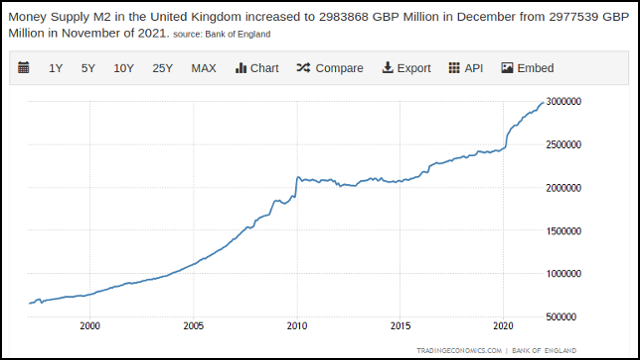

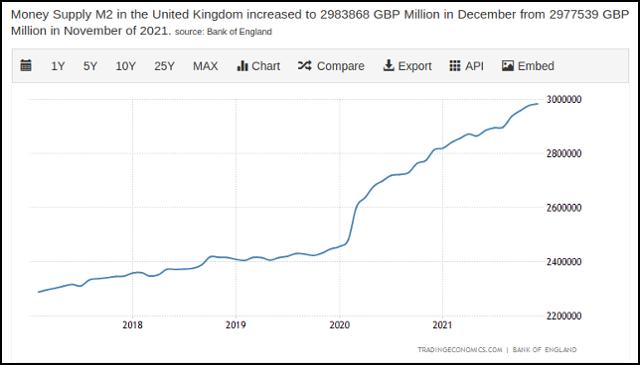

Bankers and economists often talk about the M1 and M2 measures of the total money supply. The M1 supply is a calculation that measures only the money that has the greatest liquidity. This comprises the easiest forms of money to exchange and includes cash, commercial bank deposit accounts and cheques, etc. The M2 money supply adds to that total what is held in savings deposit accounts, short-term bond funds (money market funds) and longer-term saving accounts in commercial banks. The liquidity (rapid usability) of these holdings is lower than the cash and cash-like money in the M1 calculation, but does M2 give a fuller picture of the money supply.

In February 2020, the M2 money supply stood at £2.45 trillion (one million pounds nearly two and half million times over). In response to the allegedly deadly pseudopandemic, the creation of fairy dust took off at a truly unprecedented rate. While a similar rapid spike had previously been seen—in 2010, to recapitalise the banks after their business model failed—this time the expansionary surge was prolonged.

By December 2021, M2 stood at £2.99 trillion (just under three million million dollars). In less than two years the BoE expanded the M2 money supply by approximately £540 billion. This represents more than 60% of the total £895 billion of QE that the BoE has engaged in since 2009. It is orders of magnitude greater than the QE response to the 2008 financial crisis.

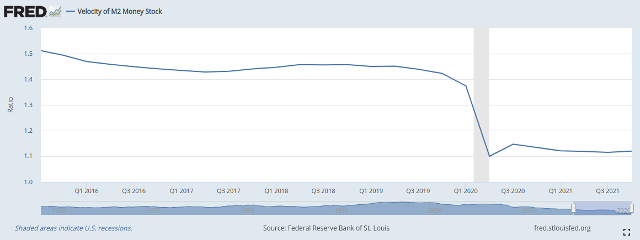

At the same time, the economy and GDP took a nose dive. However, GDP is not the only measure of economic health (or sickness). The velocity of money is a measure of how fast money is changing hands in the real economy. It shows how frequently people buy products and services in real life.

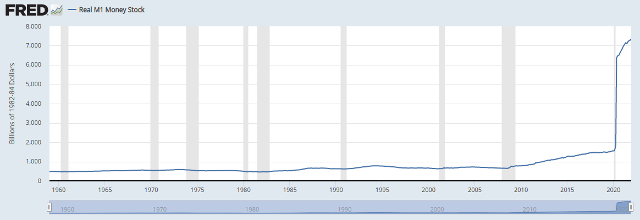

While the monetary expansion in the UK is jaw-dropping, it is as nothing compared to that seen in the world’s largest national economy, the United States. The American central bank, the Federal Reserve (Fed), expanded its M1 supply from approximately $1.6 trillion at the start of 2020 to around $7.4 trillion by December 2021.

It is crucial to note that QE on this scale doesn’t simply impact upon the economy of the nation in question. The investors who benefit from QE, in any nation, can make those investments in any other nation or multinational corporation they wish. QE has a cumulative, global effect.

Starting in the first quarter of 2020, in a time period corresponding with the announcement of the pseudopandemic, M2 velocity collapsed in the US as the economy went into lockdown. This was repeated in every locked-down country.

Yet, despite the eye-watering QE from the Fed, throughout 2021 US velocity barely recovered at all. This shows that the QE fairy dust was not going into the real economy. It was being absorbed by something else.

The first people to benefit from fairy dust inflation (“monetary expansion” to the financial establishment) are central bankers. In the both the US and the UK, electronic money printing enabled the central banks to engorge real assets.

Banks own debts, and the contracts they are based upon are assets of the banks. With national debt at more than 100% of GDP, the productive economy of the UK is effectively owned by the central bank. The UK is an asset of central bankers.

The next people down the line to benefit from the newly-created slush fund are the quantitatively-eased commercial banks.

Just as you and I bank with the commercial (“retail”) banks, so the commercial banks in turn use the services of the central banks. Commercial banks hold central bank reserves, and these determine their financial viability (liquidity). When the BoE, the Fed or another central bank engages in QE, it is boosting the central bank reserves of these commercial banks, effectively increasing their wealth and that of their shareholders.

These are the first recipients of the new fairy dust. The quantitatively-eased commercial banks are often the financiers of speculators in the financial markets. Again, the BoE is surprisingly frank about how this scam—for that is what it is—works:

Say we buy £1 million of government bonds from a pension fund. In place of those bonds, the pension fund now has £1 million in cash. Rather than hold on to that cash, it will normally invest it in other financial assets, such as shares, that give it a higher return. In turn, that tends to push up on the value of shares, making households and businesses holding those shares wealthier. That makes them likely to spend more, boosting economic activity.

It is worth being very clear about what the BoE is saying with these admissions. They illustrate why inflation is most assuredly a stealth tax and reveal who the profiteers milking the Cantillion effect are.

In a crisis, the independent, privately-owned central banks use monetary policy to “help” the economy. They do this by magically producing money out of thin air which they then feed to the commercial banks.

The private commercial banks then lend it, not to small businesses or social enterprises, but to provide finance for investors in the financial markets. Up to this point, no-one in the real, productive economy (the taxpayer) has seen a penny of this new money.

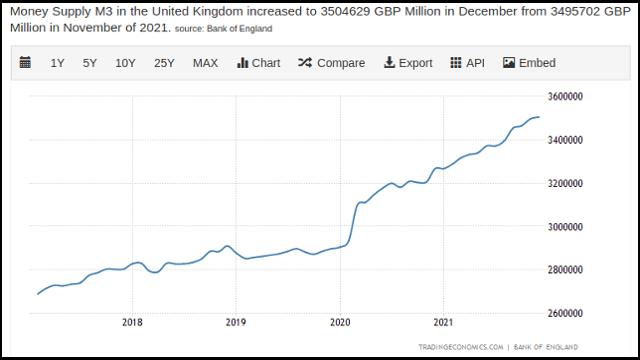

This can be observed in the UK’s figures for the size of the M3 money supply. This calculation of the amount of money in the economy adds the finances of large corporations and financial institutions to the M2 money supply. In December 2021, it stood at £3.5 trillion, thus adding an additional £510 billion of capital assets onto the balance sheets of the inflation profiteers.

Thanks to the fairy dust pouring out of the central banks, through the commercial banks and private investors, demand-pull is created in the financial markets, pushing up the price of the stocks, bonds, forex (currency) or financial derivatives that the profiteers are invested in—thus increasing profits for the already wealthy. Perhaps the beneficiaries include a few better-off “households”, but not many.

When the World Health Organisation declared a global pandemic, the stock market crashed, share prices plummeted and investors incurred losses. The BoE response was quantitative easing and the APF. This injection of zeroes bolstered the stock market and its derivatives, not the productive economy. The subsequent recovery in the FTSE 100 corresponds precisely to the size of the monetary expansion.

Inflation is the stealthy transfer of capital from the mass of the people to the select few. When the BoE board say it is “good”, they mean it is good for them and for the Global Public-Private Partnership they represent. Far from stimulating the productive economy, this new money is pumped into the financial markets, where it is siphoned off into the parallel financial dimension called the derivatives market.

A derivative is a contract to trade bundles of assets, including stocks, securities (i.e. bonds) and even commodities. The seaweed derivatives market alone is projected to be worth nearly $4 billion ($4,000,000,000) by 2027.

A derivative contract is a financial security that derives its value from the assets underpinning it. Derivatives exploit “leverage” to increase the return on fluctuations in asset prices. For example, a contract valued at £1,000 could be based upon assets worth £10,000. If the asset value increases by 1%, then the derivative trader can make 10% on their investment. Profits are amplified out of all proportion to the real-world value involved.

When the early recipients of the monetary expansion “windfall” invest their new fairy dust, they can quickly make unimaginable fortunes in the derivatives market. The derivatives market is estimated to be anywhere between $600 trillion ($600,000,000,000,000, or one million dollars six hundred million times over) and over $1 quadrillion ($1,000,000,000,000,000 or a thousand million times one million dollars). It is somewhere in the region of ten times the size of the world’s gross domestic product. To be honest, no one is really sure just how vast this fairy dust empire is.

Logically, of course, it cannot exist. A financial market ten times larger than the annual productivity of the planet is an aberration. It only exists in a digital financial world constructed from fairy dust where all money is a debt owed to the people trading in the parasitic derivatives market. As all this money inflates global asset prices, inflation starts to affect the real economy.

The window of opportunity afforded by a global Cantillion effect can be seen in the UK’s inflation figures. Despite inordinate money printing, which began in March 2020, the CPIH measure of inflation didn’t move much until March 2021–thus giving the UK0based multinational corporations and private investors a whole year to make as much profit as possible, from free money, as they sprinkled fairy dust on their portfolios.

Once the devaluation of the currency began, they had already capitalised upon the inevitable inflation. There is no windfall for us from quantitative easing. We have to work to pay the higher prices for everything. From energy and food, to raw materials and housing costs, we are now going to pay heavily for the inflation profiteering. It is a tax.

The economy is formed by real people doing real work. We produce real goods and real services from real raw materials and real energy. We trade with each other to push forward innovation, to distribute wealth; and the government forces us to pay tax to for our efforts.

By contrast, the financial markets, and the derivatives market in particular, enable those who hold capital to profit from a rigged game. Without the present-day ridiculous expansion of the money supply, there wouldn’t be enough money on Earth to sustain the game. When central banks inflate the money supply, this is where it ends up.

The derivatives market serves no useful economic purpose, and seemingly exists as little more than feeding pool for the already wealthy. Much of the debt created becomes taxpayer debt, effectively subsidising the unbridled profiteering. Meanwhile, those who benefit have enough capital to pay for the best tax avoidance schemes, such as tax-exempt philanthropic foundations.

In this system that we endure, money is created out of thin air, solely by those with the power to create it, and is repayable with interest. While both the real economy and the financial markets are currently fuelled by fairy dust, the real economy would benefit from a real currency. The non-derivative financial markets would still function, but would contract significantly.

So-called government spending, whether in response to a crisis or at any other time, is not spending. It is borrowing from central banks, commercial banks, investment funds and financial institutions. That debt is a debt we must repay. The government has no money; it simply traps us in a never ending spiral of debt and forms “partnerships” with global corporations intent upon exploiting us.

Inflation is a monetary policy decision and is the most pernicious of taxes. We are cash cows and we are being farmed. It does not have to be this way.