Part 1 of this article is here.

At the recent UN climate change summit in Glasgow, COP26, Mark Carney, the UN Special Envoy for Climate Action (previously Governor of the Bank of England), formally announced the Glasgow Financial Alliance for Net Zero (GFANZ)—first launched in April 2021 by the U.S. Special Presidential Envoy for Climate Change, John Kerry. The initial GFANZ progress reports states:

Governments must ensure a well-managed, just transition, including by working closely with industry and finance […] GFANZ was created to accelerate this process. Its goal is to transform the global financial system in order to finance the investment in a net-zero economy […] we must transition the entire financial system, alongside every sector of our economies, […] supporting frameworks and metrics to measure portfolio and sectoral net-zero alignment.

While the rather speculative claims of GFANZ grabbed all the headlines, the next person on the COP26 stage following Carney was Erkki Liikänen, the chairman of the International Financial Reporting Standards (IFRS) Foundation. He proclaimed the creation of the International Sustainability Standards Board (ISSB). In doing so he established the “basis for action”—precisely as prescribed by the UN three decades earlier.

The ISSB delivers on the globalist agenda outlined in UN Agenda 21. It creates the asset rating system that will see a global partnership of stakeholder capitalists assume control of every resource on Earth. This economic regime will sit within a new international monetary and financial system (IMFS) that will enable the stakeholder partners to centrally plan the global economy and manage every aspect of it.

In the first part of this article, we discussed how a Global Public-Private Partnership (G3P) had seized upon the “opportunity” of the pseudopandemic to embark upon this transition. In August 2019, the gathered G7 central bankers at Jackson Hole, Wyoming, admitted that the existing IMFS was finished and that there was an urgent need to construct a new one, as “the centre won’t hold”.

The global investment firm BlackRock, which appears to own a large share in the major central banks, introduced the joint fiscal and monetary concept of “going direct”. In the document they presented at Jackson Hole, BlackRock outlined what “going direct” would mean politically:

Going direct means the central bank finding ways to get central bank money directly in the hands of public and private sector spenders […] Going direct […] works by: […] enforcing policy coordination so that the fiscal expansion does not lead to an offsetting increase in interest rates.

In this article, we are going to explore the immense economic and financial implications of BlackRock’s plan, which has been set in motion and is currently operating globally. It stipulates that central banks—which are privately owned—control our governments' fiscal policy and that policy coordination is enforced. In other words, central banks, and ultimately private wealth managers, will control the spending of our taxes and of the debt taken out in our and our children's name.

This is a global coup d’état. The government you elect no longer controls how it spends your taxed income; central banks do, and they will do as directed by private money.

We currently endure taxation without representation. However, to fully grasp the global scale of the revolution, we need to understand the G3P, which we covered in Part 1 of this article.

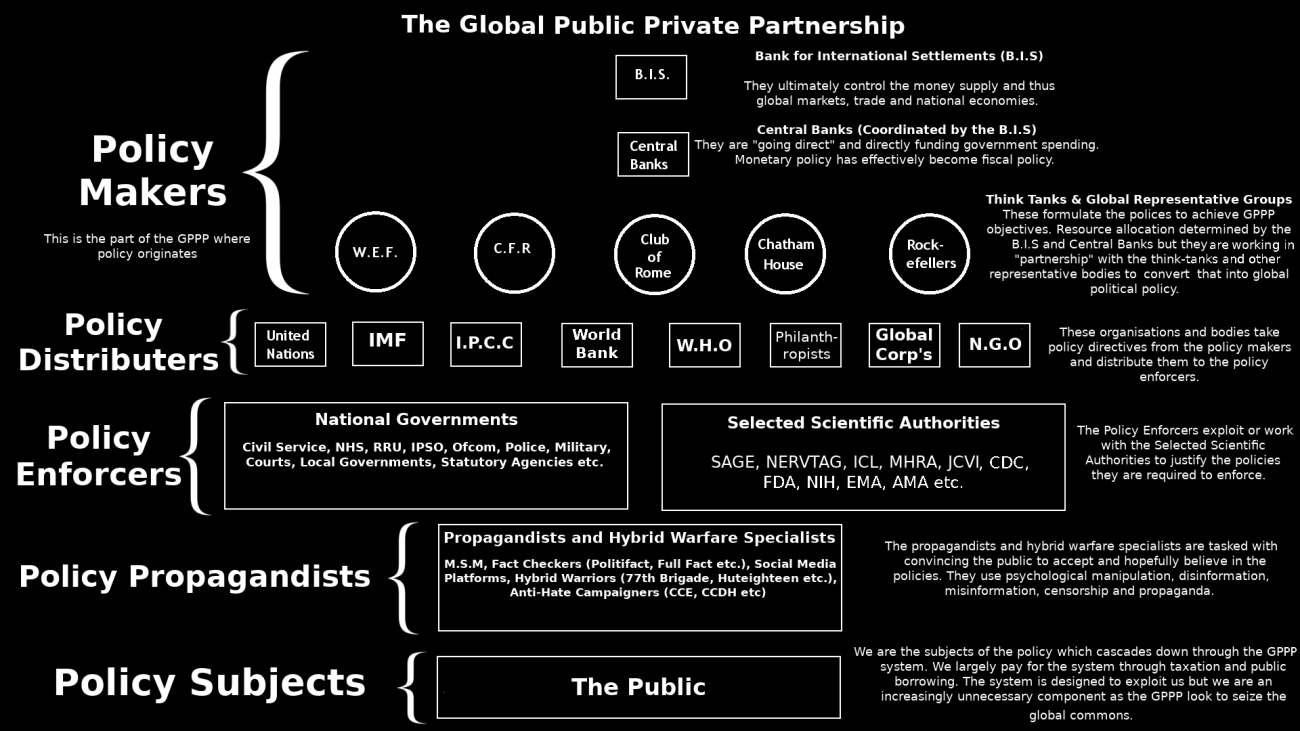

The Global Public-Private Partnership (G3P)

As a brief reminder, the Global Public-Private Partnership is a worldwide network of corporations, privately funded think-tanks, intergovernmental organisations, financial institutions, non-governmental organisations, philanthropic foundations (together with their respective trusts), governments, selected academic institutions, civil society groups, media organisations and private investors. It is a hierarchical, compartmentalised, authoritarian structure.

Its activities are sometimes referred to as the “international rules-based system”. The G3P controls the flow of policy around the world.

In this fluid model of global governance, global think tanks coordinate and develop policy agendas in partnership with central banks, the Bank for International Settlements (BIS) and other key stakeholders. Intergovernmental organisations and global financial institutions then promote the agenda before national government (enforcement partners) convert it into hard policy and often legislation.

Policy propagandists, such as the mainstream media and hybrid warfare specialists, then sell the policy to the public. We are then subjected to the policies that originated at the global—G3P—governance level.

Power over the entire system is maintained by the central banks and ultimately by the BIS. As the only people on Earth with the power to create money from nothing, even prior to the pseudopandemic, their ability to shape global investments and markets, and consequently steer the world economy, has long been significant. The Covid-19 crisis provided the catalysts to convert that influence into direct control.

Professor Richard A. Werner empirically proved that money is created from nothing by commercial banks when they make a loan. He showed that all "broad money" (the money you and I use every day) is debt. This commercial money creation process can be called the monetisation of debt.

Commercial banks hold central bank reserves using a different form of money called base money. They settle accounts with each other at the central banks. Their pay using their base money reserves in a process called interbank settlement. In turn, central banks operate the same settlement system with each other, settling accounts, using base money, at the BIS (hence its name).

As John Titus demonstrates, these two monetary circuits, the broad and base money circuits, existed separately (in theory), prior to the implementation of “going direct.” BlackRock’s plan has changed this, enabling central banks to feed base money into the broad money circuit, essentially to drive the financial markets.

However, central banks create (base) money from nothing in the same way that commercial banks do. They also monetise debt, often by trading government securities (bonds), guaranteed by our future taxes.

Money creation essentially boils down to typing some numbers into a digital accounts ledger. This is what commercial banks do when you “deposit” a loan with them and it is what central banks do when they trade bonds.

Prof. Werner aptly referred to this debt monetisation process as the creation of “fairy dust”. This power to create money from absolutely nothing had hitherto been the sole province of commercial and central banks and the BIS. The impending creation of central bank digital currency (CBDC) will further consolidate and centralise this authority into the hands of the central banks and the BIS alone.

The magic power of money creation is that it enables the G3P to seize the global commons (definition below). In doing so, they are taking for themselves every resource on Earth and establishing centralised, systemic control of the entire global economy.

Setting the Global Policy Agenda

In 1972, the privately-funded G3P policy think tank, the Club of Rome, published Limits To Growth. On the basis of what was spat out of the Massachusetts Institute of Technology’s (MIT) system-dynamics model, World3, and a whole raft of assumptions fed into it, the Club of Rome concluded that the world was doomed because there were too many people living on it. This caught the public imagination: long before Professor Neil Ferguson, it was perhaps the first time that a speculative computer model, with questionable parameters and inputs, would be used to shape global policy.

Wrongly assuming that humanity is nothing more than a drain on resources, the Club of Rome went on to describe how there would be uncontrolled war, pestilence, plague and famine unless something was done about population growth. Their MIT-commissioned computer model told them that the world would collapse shortly after the year 2000. The only way to save the Earth was to start getting rid of people.

Building upon their many errors, they envisaged a global state of “equilibrium” where resource use and productivity were balanced to provide a sustainable™ future for all of humanity. They decided this could best be achieved by ridding the planet of most of the people living on it:

It is possible to alter these growth trends and to establish a condition of ecological and economic stability that is sustainable far into the future. The state of global equilibrium could be designed so that the basic material needs of each person on earth are satisfied […]

Although the effort may initially focus on the implications of growth, particularly of population growth, the totality of the world problématique will soon have to be addressed […] It may be within our reach to provide reasonably large populations with a good material life.

Two Club of Rome members, the former Norwegian Prime Minister Gro Harlem Brundtland and the then Secretary-General of the UN, Javier Pérez de Cuéllar, were instrumental in the formation of the Brundtland Commission in 1983. In terminology lifted directly from the Club of Rome's Limits of Growth, their goal was to investigate and report upon the “global problématique”.

They published Our Common Future (the Brundtland Report) in 1987. Sticking firmly to the flawed assumptions in Limits To Growth, the report stated:

Excessive population growth diffuses the fruits of development over increasing numbers instead of improving living standards in many developing countries; a reduction of current growth rates is an imperative for sustainable development […]

However [in the sense of 'in whatever way'] a nation proceeds towards the goals of sustainable development and lower fertility levels, the two are intimately linked and mutually reinforcing.

The problem for the G3P depopulation enthusiasts was that this sustainable future was a hard sell to the global population they intended to reduce. Nothing daunted, further Club of Rome deliberations produced a solution to the marketing problem. In 1991, in their publication The First Global Revolution, the enthusiasts wrote:

In searching for a new enemy to unite us, we came up with the idea that pollution, the threat of global warming, water shortages, famine and the like would fit the bill […]

All these dangers are caused by human intervention and it is only through changed attitudes and behaviour that they can be overcome […]

The real enemy, then, is humanity itself.

After nearly two decades being kicked around the G3P think tanks, the policy agenda finally had a basis for action: humanity was the enemy of itself, and ecological and economic sustainable development required attitudes and behaviours to be changed globally.

The 1992 Rio Earth Summit gave rise to Agenda 21. This is the G3P's 21st-century plan for the transition to a new form of worldwide, sustainable society. It led to the United Nations Environmental Programme’s Millennium Development Goals (MDGs), which were updated to become Sustainable Development Goals (SDGs) under UN Agenda 2030.

In the UK, the local enforcement partner, HM Government, converted the global policy agendas, which stemmed from the Club of Rome, into SDG-based net zero policies. This is how the compartmentalised, hierarchical authority of the G3P system works.

It enables the schemes of billionaire philanthropists, and other key G3P stakeholders, to be translated into policies and laws which impact upon each of us. We elect our own enforcement officers; we don’t affect the policy agenda.

Converting Nature into Ecosystem Services

In September 2021, the New York Stock Exchange (NYSE) announced a whole new type of asset class. The NYSE developed this class in partnership with the Intrinsic Exchange Group (IEG), whose founding investors include the Rockefeller Foundation.

The idea of this novel asset class is that owners of natural assets, such as farmers, conservation trusts, governments, etc., will be able to create an investment vehicle as a specialised corporation, one which holds the rights to “ecosystem services”. Carbon sequestration (afforestation) or clean water supplies, for example, will be the “assets” which determine the value of a member of this asset class, the Natural Asset Company (NAC).

Investors, such as private investors (individuals and institutions), corporations, sovereign wealth funds and multilateral development banks, can then “buy the assets” registered to the NACs. By converting nature and all natural resources into financial assets, the operators of this scheme enjoy seemingly boundless investment opportunities. Even so, the IEG’s claim for the potential scale of this new global market is still staggering.

The IEG states that the purpose of the new asset class and its NACs is “the conversion of natural assets into financial capital”. The ambition, as expressed by the IEG, is so gargantuan as almost to defy comprehension:

We are pioneering a new asset class based on natural assets and the mechanism to convert them to financial capital. These assets are essential, making life on Earth possible and enjoyable. They include biological systems that provide clean air, water, foods, medicines, a stable climate, human health and societal potential. The potential of this asset class is immense. Nature’s economy is larger than our current industrial economy and we can tap this store of wealth.

According to the IEG, the current asset value of the world’s economy is $512 trillion, including all financial derivatives. The projected value of assets in the new economy they are creating is said to be worth eight times that: an estimated $4,000 trillion (four quadrillion dollars, or $4,000,000,000,000,000.) The solution to climate change is a market opportunity unlike any ever seen in human history.

The G3P has decreed that nature is now an “ecosystem service”. The cycle of life itself is a “product”. Everything that is currently “owned” by human beings, both publicly and privately, is to be included in the capitalisation process. The IEG adds:

On public lands, natural asset owners are typically government actors […] on private lands, asset owners are typically private farmers, ranchers, or forest property owners […]

Natural Equity is a store of value like any other security or monetized asset. The stocks of water, timber, biodiversity, soil, carbon, fish or other natural assets make life on Earth possible and are thus the ultimate store of value for investors.

There are also vast swathes of the Earth, such as the deep oceans, Antarctica and the atmosphere, that are not “owned” by anyone. In a telling reference to commons—local lands which peasants in the past could all graze their sheep on (until the lands were seized piecemeal by the élite)—these are now dubbed the “global commons”. The IEG is among the G3P stakeholder partners who, in addition to capitalising all that is owned, intend to capitalise all that is not owned:

Though some services, like freshwater production may be monetized directly, most ecosystem services currently are not […] The equity of a Natural Asset Company captures all of the above elements of value, creating financial realization via a security, whereby the full value of natural assets is priced in a market transaction.

The G3P is attempting the seizure of everything, of all resources owned and those which “currently” are not. This is a gambit for total dominion over the planet.

The reason why we are now told we will own nothing is that private investors will own everything. Nature will no longer be the environment which “makes life on Earth possible” but rather an “ecosystem service” which creates a “store of value for investors”.

The Basis for Action

Like COP26, the 1992 Rio Earth Summit was a policy showcase. The policies had already been decided; the summit simply allowed the framers to receive some fanfare and to be histrionically berated by a proto-Greta upon their official launch. One of the documents issued at the Rio Summit was Agenda 21. The preamble stated:

Humanity stands at a defining moment in history. We are confronted with […] the continuing deterioration of the ecosystems on which we depend for our well-being. However, integration of environment and development concerns and greater attention to them will lead to […] better protected and managed ecosystems and a safer, more prosperous future. No nation can achieve this on its own; but together we can—in a global partnership for sustainable development.

At section 8.41, Agenda 21 declares what is described as the “Basis for Action”:

A first step towards the integration of sustainability into economic management is the establishment of better measurement of the crucial role of the environment as a source of natural capital […]

A common framework needs to be developed whereby the contributions made by all sectors and activities of society, that are not included in the conventional national accounts, are included […]

A programme to develop national systems of integrated environmental and economic accounting in all countries is proposed.

Thirty years ago this year, the UN stakeholders agreed the first step needed for the global partnership to transitioning us all into the new global economic system. This required the establishment of some measurement of the environment as a form of natural capital.

It was anticipated that that would have to include an accountancy system for the global commons, as this was “not included in the conventional national accounts”. For example, Agenda 21, section 17.1, speaks about the global commons of the deep sea. It describes the world’s oceans as:

An integrated whole that is an essential component of the global life-support system and a positive asset that presents opportunities for sustainable development.

Agenda 21 stipulated that once nature had been capitalised, all countries would adopt a common framework that would enable them to combine environmental accounting with economic accounting systems.

This is exactly what Erkki Liikänen announced at COP26. While his speech garnered far less media attention than Carney’s, it was the Finn who spelled out how the new global economy will be run, and by whom.

As discussed in Part 1 of this article, the World Economic Forum has published a paper creating the concept of the Environmental, Social and Governance (ESG) rating for financial assets, forming part of what the WEF referred to as stakeholder capitalism metrics.

Numerous ESG ratings subsequently emerged through the ratings agencies, rapidly rendering the system unwieldy. In June 2021, the WEF convened its International Business Council (IBC) to work with the global Big Four accountancy firms, Deloitte, EY, KPMG and PwC, to formulate twenty-one core ESG metrics.

Also at COP26, Liikänen announced the creation of the International Sustainability Standards Board (ISSB). He stated the purpose of the ISSB as follows:

To develop, in the public interest, a comprehensive global baseline of sustainability disclosures for the financial markets, IFRS Sustainability Disclosure Standards […]

The ISSB will sit within the IFRS Foundation, alongside the IASB, and will work closely with it […]

Its standards will help investors understand how companies are responding to ESG issues, like climate, to inform capital allocation decisions.

The International Financial Reporting Standards (IFRS) Foundation sets accountancy standards for governments, other public institutions and private companies the world over. They have financial authority in 140 jurisdictions, including the USA, the EU, the UK, Canada, Australia, New Zealand, China and Russia. They present themselves as a quasi “not-for-profit, public interest” authority. They are not any such thing:

Our Standards are developed by our two standard-setting boards, the International Accounting Standards Board (IASB) and the newly created International Sustainability Standards Board (ISSB). The IASB sets IFRS Accounting Standards and the ISSB sets IFRS Sustainability Disclosure Standards.

The International Accountancy Standards Board (IASB) is a private-sector organisation representing private stakeholder capital interests, not the public interest. The ISSB will “work closely” with the private IASB to set “Sustainability Disclosure Standards”. For its part, the ISSB states:

Strategic advice will be provided by the IFRS Advisory Council.

The IFRS Advisory Council is a global public-private partnership between governments, intergovernmental organisations, private corporations, global financial institutions, central banks, NGOs and private investment groups. It is chaired by Bill Coen, the former Secretary-General of the Basel Committee on Banking Supervision—which is part of the Bank for International Settlements.

PwC is represented on the IFRS Advisory Council by its Global Chief Accountant, Henry Daubeney. Following Liikänen’s announcement, PwC's UK Head of Audit, Hemione [sic] Hudson, said:

The launch today of the International Sustainability Standards Board is an important step towards achieving a global common approach to ESG-related disclosure standards. Harnessing the power of the financial markets to play a leading role in the transition to a net zero economy […] Reporting standards are a critical component to achieving this.

The Financial Stability Board (FSB) secretariat is “hosted” and funded by the Bank for International Settlements (BIS). It is based at BIS headquarters in Basel, Switzerland, in a building which enjoys diplomatic immunity. Mark Carney was Chairman of the FSB in 2015. At the Paris COP21 summit, a precursor to Glasgow COP26, he launched the the FSB’s task force on climate-related financial risks:

The Task Force on Climate-related Financial Disclosures (TCFD) will develop voluntary, consistent climate-related financial risk disclosures for use by companies in providing information to lenders, insurers, investors and other stakeholders.

In October 2021 the UK Government announced that, by April 2022, it will be mandatory for approximately 1,300 of the UK’s largest companies to submit their Climate-related Financial Disclosures. The plan is to extend this requirement to all businesses by 2025. Similar mandates are being imposed by other European governments. The UK Government has produced a roadmap towards mandatory climate-related disclosures:

The Roadmap presents a coordinated strategy for seven categories of organisation: listed commercial companies; UK-registered companies; banks and building societies; insurance companies; asset managers; life insurers and FCA-regulated pension schemes; and occupational pension schemes. A coordinated approach across the economy will help to ensure that the right information on climate-related risks and opportunities is available across the investment chain.

Just what constitutes the right information to divulge will be determined by the private ISSB, based upon the core ESG metrics defined by the G3P stakeholder capitalists. This will give the G3P control over global investment flows, as investors surge towards the companies with high ESG ratings and avoid, claiming this to be a fiduciary duty, those who have failed to adapt to the new low carbon economy. As Mark Carney said in July 2019:

Companies that don’t adapt—including companies in the financial system—will go bankrupt without question. [But] there will be great fortunes made along this path aligned with what society wants.

This is not what society wants; society hasn’t been asked. Carney was threatening global business, but also highlighting the untold profits to be made by those willing to redefine nature as an ecosystem service.

In a rollout starting with developing nations (of course), Natural Asset Companies (NACs)—or some future ESG investment vehicle yet to be devised—will hoover up every natural resource on Earth. They will have “the rights” to the world's ecosystem services, such as rare earth metals, forests, farms and sources of fresh water.

Natural capital assets will also be rated using ESG benchmarks, overseen by the G3P’s ISSB. Business isn’t choosing to adapt; it is being forced to adapt. So-called sustainable development is an authoritarian command to engage in a global resource heist.

The companies which enjoy the G3P's grace and favour will do very well; those that don’t will go bankrupt (Carney's own threat). Having friends in high places will be essential in the new net zero global economy.

The G3P New World Order

Climate change activists such as Greta Thunberg and the leadership of Extinction Rebellion are demanding a new carbon reset global economy. They are advocating the creation of a new world order which will be under the compartmentalised, hierarchical authority of the G3P.

The mainstream media glitterati parroted the mantra that COP26 was a failure. Like the leading activists they support, they still fondly imagine that climate summits are about “saving the planet”. They are not, and they never were. They are about creating a new global economy—and, beyond the GFANZ headlines, Erkki Liikänen’s ISSB announcement was a global game changer.

Xi Jinping’s absence from COP26 may have been sold to us as betokening China’s lack of interest in climate change, but the People's Republic of China very much is interested in the G3P’s new global economy. No sooner had Liikänen made his announcement than the PRC Ministry of Finance wrote to the IFRS offering to host the ISSB:

Developing one single set of high quality, understandable, enforceable and globally accepted sustainability standards by the ISSB is of great significance.

Via its control of ESG asset ratings, the G3P is devising an entirely new international financial system. Yields obtained will depend upon the subjective judgements of the upper echelons of the G3P. Going direct enhances control, as central banks and the BIS directs their G3P government partners to enforce the globally accepted sustainability standards.

COP26 fulfilled all the BIS' expectations. For the Global Public-Private Partnership, COP26 was a roaring success.

Central Bank Digital Currency

Controlling investment, defining markets and directing the activities of all business is a strategy that ensures the successful manipulation of supply side of the economic model; but in order to have total control of the global economy, the G3P also needs to rig the other side of the equation: to set market demand and to adjust it to order. Thus, central bank digital currency (CBDC) will complete the transformation.

In January 2021, the BIS published Ready, Steady Go? – Results of the third BIS survey on central bank digital currency. It stated:

Most central banks are exploring central bank digital currencies (CBDCs), and their work continues apace amid the Covid-19 pandemic. As a whole, central banks are moving into more advanced stages of CBDC engagement, progressing from conceptual research to practical experimentation.

The BIS and its central bank G3P partners propose two types of CBDC: retail (broad money) and wholesale (base money).

The BIS intends to forego the opportunity that presents itself to rid the world of the system of split monetary circuits that has led to a global debt of $72 trillion. Instead, it will plough ahead with Going Direct, maintaining the split circuit for the purposes of controlling global debt while simultaneously fusing the two for the purposes of managing the global money supply directly. A split split-circuit model, if you like.

As described by Richard D. Hall, in the CBDC monetary system, central banks will henceforth not only control interbank settlement (oversight of all commercial banks) but also the supply of money to every human being on Earth (population oversight). The initial objective is to support financial markets. The ultimate goal is to institute monetary slavery.

The BIS claims that:

CBDC is central bank-issued digital money […] it represents a liability of the central bank […] CBDC is intended to be a digital equivalent of cash for use by end users (households and businesses), it is referred to as a ‘general purpose’ or ‘retail’ CBDC.

The key to seeing through the BIS deception is the admission couched in the phrase “liability of the central bank”. That liability is the legal responsibility of the central bank. People are not liable for what they do not own. It is their liability: the CBDC belongs to them, not you.

While the Bank of England and the UK Treasury have merely stated their intention to spell out the case for CBDC in 2022, China has already introduced its digital yuan. PRC state officials claim 1.4 million people have opened state-controlled digital wallets, with more than $9.7 billion worth of transactions already concluded using the new Chinese CBDC.

Because CBDC is purely digital, it has also been called “programmable money”. The BBC explained what this would mean for us:

Payments could be integrated with appliances at home or tills at the shops. Tax payments could be routed to HM Revenue and Customs at the point of sale […] electricity meters paying suppliers directly […] allowing payments such as for a few pence each time to read individual news articles.

Other suggested uses for CBDC include progressively reducing the balance of your wallet to encourage spending, or adding surcharges to transactions to reduce economic activity. CBDC will be built on a blockchain but—unlike cryptocurrencies, which rely upon an anonymous network of nodes to independently validate transactions—CBDC blockchain gateways will be tightly monitored and controlled by the central banks.

This will afford the central banks comprehensive surveillance of every transaction. Your jurisdiction's central bank, or rather its AI algorithms, will have the ability to permit or deny your transaction at the point of sale. Speaking to the virtual IMF and World Bank annual meeting, the General Manager of the BIS, the foursquare Augustín Carstens, could barely contain his excitement:

CBDC […] will be the third type of liability of a central bank […] we tend to establish the equivalence with cash and there is a huge difference there. For example, in cash we don’t know for example who is using a $100 bill today […]

A key difference with the CBDC is that the central bank will have absolute control on the rules and regulations that will determine the use of that central bank liability, and also we will have the technology to enforce that […]

I think this is good news.

CBDC will also bolster G3P control of global markets. Given the central banks' added power to control all payments, investors who contemplate backing a venture of which the G3P does not approve could find it technologically impossible to make that investment. When this is combined with ESG ratings for natural assets (ecosystem services), the G3P's financial and economic control of the world will be absolute.

This is all good news for the G3P new world order. Once central bank digital currencies are our only source of money, we will never have financial freedom again. We really will “own nothing”—but not because we are committed to reducing our carbon footprints.

It will be because the G3P owns everything; something which will make them very happy.