No new technology is good or bad in itself, and only its application can and will determine whether we should embrace or resist its implementation. I can’t quite remember how mobile phones were sold to us all those years ago, beyond the promises of convenience, progress and a competitive edge; but I don’t recall being told they would become the tracking devices for a system of surveillance and control that is becoming increasingly hard not to describe as ‘totalitarian’.

Neither does the application of new technology exist in isolation from other technologies and other programmes. What I want to do in this article, therefore, is to discuss the contexts—economic, social, political and environmental—in which Central Bank Digital Currency is, in the parlance of our day, being ‘rolled out’.

The avid promoters of CBDC, including our unelected Prime Minister, Rishi Sunak, say very little about its necessity, applications and benefits beyond similar claims of progress, of fighting financial crime—which would be a first for the Bank of England—and, of course, of sustainability, which is now the justification for every new removal of a human right or civil liberty. But the wider and expanding contexts of the Global Biosecurity State, I believe, give us a more accurate understanding of the real application of Central Bank Digital Currency and, indeed, of its intended purpose.

1. Is it Programmable?

CBDC is digital or electronic money for households and businesses alike. The Bank of England, which calls it the ‘Digital Pound’, says CBDC is not a cryptocurrency like Bitcoin, because it is not privately issued, but instead a ‘liability’ of the bank, and will therefore retain its value over time, rather than being subject to rapid fluctuations in value as happens with investments in crypto-assets.

Significantly, the Bank of England describes CBDC as the ‘safest’ form of money available: a value with the greatest currency in the Global Biosecurity State. If—or, more accurately, when—it is implemented, the Bank of England will make central bank money available to the public in digital form for the first time. As of last November, the Bank of England insists that CBDC will not replace but, instead, ‘exist alongside cash and bank deposits’.

The Bank of England published its first paper on CBDC in March 2020—coincidentally, the same month that lockdown restrictions were imposed on the UK, largely closing down the real economy for the next two years. The Chancellor of the Exchequer (British finance minister), who at the time was Rishi Sunak—another coincidence—set up a CBDC Taskforce in April 2021, shortly after the second spike in UK deaths attributed to Covid–19.

This joint taskforce between the Treasury and the Bank of England is working with the central banks of other countries and states, as well as with the Bank for International Settlements—about which more later. The same month, the Bank of England set up two forums, one for CBDC technology, the other for CBDC implementation and operation. These include its use, functions, the role of the public and private sectors; its implications for data privacy; and what the Bank of England, with a nod to the newly enforced orthodoxies of woke, calls financial and digital ‘inclusion’. By this, they do not mean how everyone will have access to this wonderful new advancement in digital technology, but rather how everyone is going to be forced to adopt it.

In June 2021, Tom Mutton, the Director of the Bank of England’s Central Bank Digital Currency unit, addressed why we need another form of digital money to that already offered by the private sector. One of the reasons, apparently, is to avoid the risks presented by new forms of private money creation like Bitcoin. Another is improving the availability and usability of central bank money to all British citizens. Another is building a platform for better cross-border payments. Another is what he claimed is the greater efficiency of the Digital Pound when compared to the energy costs of Bitcoin, which the Agenda 2030-compliant G7 nations have said should be a core consideration in CDBC design. The rest of the reasons enumerated were vague promises about meeting future payment needs in a digital economy and the apparently complete natural and not at all managed decline in the use of cash.

Of more interest than Mutton’s touting of these apparent benefits was his admission that CBDC ‘could support wider public policy objectives’, which is a new concept in money. Germane to this new role of money as policy supporter is CBDC technology, which allows it to be ‘programmable’. By this, Mutton means that transactions using CBDC can occur (or not occur) automatically ‘according to certain conditions, rules or events’. So how is this going to work?

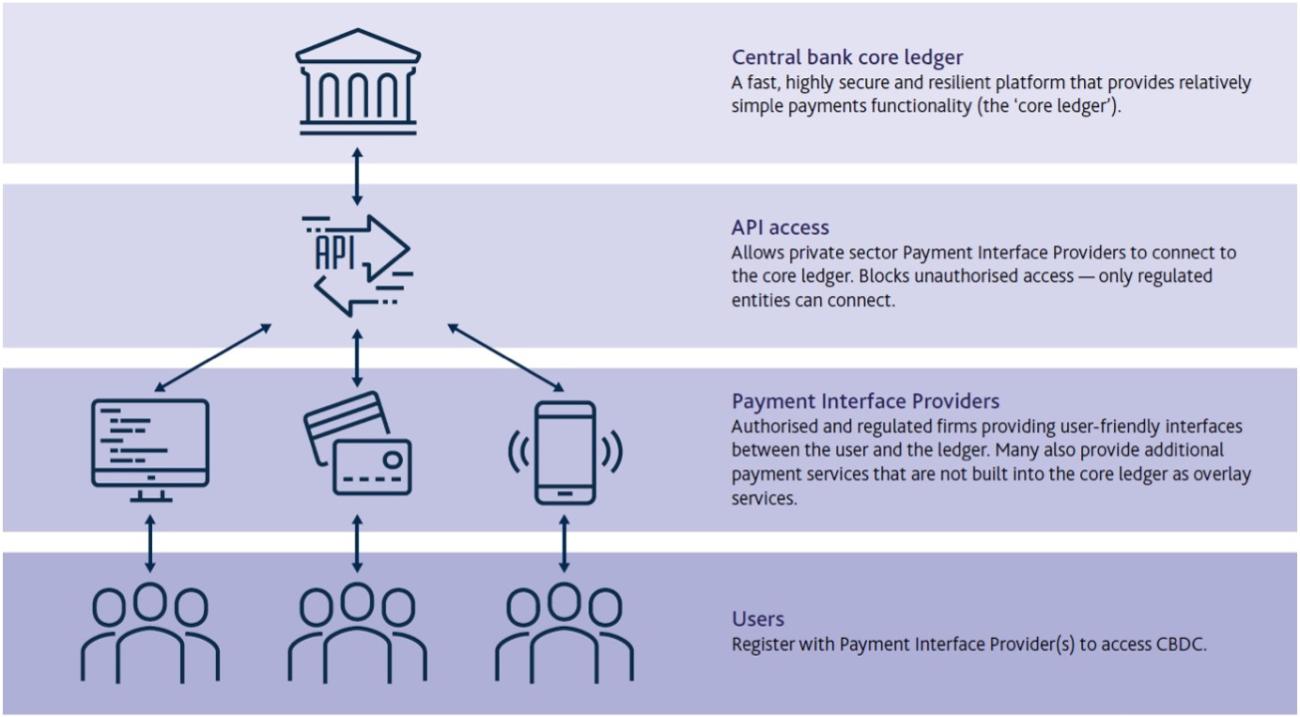

The proposed architecture of CBDC is that, at the top,

- the Central Bank core ledger is accessed via

- an Application Programming Interface (API) that regulates and authorises

- private Payment Interface Providers (PIPs), through which

- registered users at the bottom can access Central Bank Digital Currency.

Importantly, the API is different from a user interface, in that it connects computer programmes, not a computer to a person. It also hides the internal details of how a system works.

The Bank of England claims that it will not be able to programme our money or how we spend it. However, it adds that, if and when CBDC is introduced, the programmability features will be designed by the private sector companies providing the Payment Interface. Last July, the Deputy Governor of the Bank of England, Jon Cunliffe, who is overseeing the Bank of England’s work on central bank digital currencies, confirmed that this interface with the public will be provided by commercial banks.

In the UK, where five banks account for 90 per cent of all deposits, that means in effect HSBC Holdings, the Lloyds Banking Group, the NatWest Group, the Royal Bank of Scotland Group and Barclays. But, as the Bank for International Settlements indicated in its report published in September 2021 on the system design and interoperability of CBDC, Payment Interface Providers might also include Big Tech companies: Alphabet (Google), Amazon, Apple, Meta (Facebook) and Microsoft.

Passing the buck on what this will mean in practice, in June 2021 the Bank of England called on government ministers to decide whether CBDC should be ‘programmable’, and therefore giving the issuer control over how it is spent by the recipient. Mutton commented:

There could be some socially beneficial outcomes from that, preventing activity which is seen to be socially harmful in some way; but at the same time it could be a restriction on people’s freedoms.

As well as being a means to ‘support’ public policy objectives therefore, it appears CBDC will also be a means to ‘prevent’ actions of the public deemed to be harmful. As the last three years have demonstrated and the Online Safety Bill will write into legislation, that includes questioning the Government on anything from the dangers of experimental gene therapies to the tenets of environmental fundamentalism.

This is the context in which we should understand what a ‘restriction’ on our freedoms means. No wonder that an anonymous spokesman for the Treasury confirmed: ‘Programmability is a potential feature of a Central Bank Digital Currency’. From what its designers and promoters have said, I’d say it was the primary feature.

Tom Mutton also highlighted that the problem of how users identify themselves—and in doing so ensure the ‘inclusivity’ of CBDC for every lucky citizen—would be solved by a system of Digital Identity. He framed this in terms of a ‘trade-off’ between the privacy of the users and the security of CBDC against financial crime.

He admitted that this will, regrettably but inevitably, entail sharing information about the identity of the users with the Payment Interface Providers, who would therefore be responsible for security and also for the privacy and uses of the user’s personal data. We’ve already had numerous examples of where this leads—most famously demonstrated by the agreement between Facebook and the UK private intelligence company Cambridge Analytica—which is to the market sale of our private data by information technology companies to the highest bidder.

It sounds very much, therefore, as if Central Bank Digital Currency cannot be implemented without Digital Identity, and that Digital Identity is being justified by, among other programmes, the joys and benefits of CBDC. It is not by chance that, the same week the Government published its consultation on the Digital Pound, it also published its consultation on Digital Identity. Neither initiative actually asks the British public whether it wants either.

Today, of the 119 currencies whose managers are considering implementing CBDC, it is actively being researched in 39 of them; in 33, including the UK, the USA, the eurozone, Japan, Brazil and Canada, it is being developed; 17, including China, India, Saudi Arabia, South Africa, Russia and the Ukraine, have a pilot scheme; and 11, including the Bahamas, Jamaica and Nigeria, have already launched it.

This month, February 2023, the Bank of England and the Treasury together announced that a Central Bank Digital Currency will be launched in the UK this decade, and be operational by 2025 at the earliest. Suggestively, it proposed limiting individual holdings of digital ‘wallets’ to between £10,000 and £20,000, with the former limit accommodating the existing balance, salary and bonuses of 75 per cent of the UK population, and the latter limit 95 per cent. This doesn’t sound like a currency that will exist ‘alongside’ cash.

Finally, in the Consultation Paper jointly published by the Bank of England and the Treasury this month, and which stretches to over 100 pages, only one (page 79) mentions the question of ‘programmability’, where it states:

We do not propose to develop a digital pound that enables government or central bank-initiated programmable money [. . .] While it may be possible to program the digital pound so that it could only work in certain ways, this is not relevant to HM Treasury and the Bank’s policy objectives for the digital pound.

However, HM Treasury and the Bank would permit Payment Interface Providers and External Service Interface Providers to implement such functionalities themselves, but they would require user consent and not be at HM Treasury or the Bank’s direction.

More about this is said in the Bank of England’s accompanying Technology Working Paper, in which it proposes (on page 76) the use of ‘smart contracts’ that provide ‘API access to locking mechanisms with configurable conditions on the core ledger’. This locking mechanism would require:

- ‘earmarking funds with set conditions on when the funds can be released’;

- ‘programming the earmarked funds to only release the payment when a linked event has completed conditions under the contract or programmed rules.’

The way the Bank of England has presented the programmability function of CBDC to the British public is as a means to check and transfer funds to our Digital Pound balance, purchase goods with a smartphone, pay for services, order commodities online, and allocate funds to pay our rent, standing orders and other regular payments. Ease and convenience.

So, nothing to worry about then! The Bank of England and the Treasury won’t programme its digital currency with rules—but the commercial banks and information technology companies providing the Payment Interface through which we use it can, including by contracted conditions of use which, if not met, activate a locking mechanism between us and the core ledger of Central Bank Digital Currency.

But only, apparently, if we want it. What could possibly go wrong?

2. Other Programmes of the Great Reset

With such assurances from the Bank of England and HM Treasury, what are the worries and fears about Central Bank Digital Currency, and should we listen to them? These can be summed up with the argument that CBDC is not being put forward in isolation but as part of a revolutionary change, not only in the technologies of what is being called the Fourth Industrial Revolution, but also in the programmes implementing them. It is only by looking at these programmes, therefore, that we can grasp the economic, political, social and, as we’ve seen, environmental contexts in which CBDC is being developed, will be implemented and, eventually, become operative within the next five years or so.

It’s unlikely, to put it mildly, that the huge work of building the technology for the Digital Pound on which the Bank of England has embarked will be rejected by HM Treasury when it’s completed. How, then, are they going to implement it against the expected resistance? The simple answer is, in conjunction with the technologies and programmes of the Global Biosecurity State and the regulations and restrictions that enforce them.

Implemented as mere upgrades to the infrastructure of the nation state, these will fundamentally and perhaps irreversibly change the social contract between the citizen and the state, and with it the ability of the ruled to scrutinise, influence or hold their rulers to account. Largely unknown to a general public preoccupied with pronouns, the Royal Family, hugging Volodymyr Zelenskyy and alien invasion, these include, but are not limited to, the following.

Digital Identity, holding our biometric data and monitoring our compliance with the constantly-updated requirements to be injected as many times and with whatever the state tells us made a condition of access to the rights of citizenship. This will include our freedom of movement and, under future manufactured ‘crises’, our freedom of association and assembly—and perhaps, if the fundamentalists have their way, our right to education, work, medical treatment and liberty.

In October 2019, the World Bank proposed acting as a central repository of data relating to the good practices of countries implementing Digital Identity, facilitating the transfer of information to interested parties and incentivising compliance with preferential loans and grants. Digital ID is the gateway to the enforcement of all the other programmes. Indeed, in May 2021 the Financial Times reported:

What CBDC research and experimentation appears to be showing is that it will be nigh on impossible to issue such currencies outside of a comprehensive national digital ID management system. Meaning: CBDCs will likely be tied to personal accounts that include personal data, credit history and other forms of relevant information.

Universal Basic Income for the millions of workers, primarily from white-collar jobs, made redundant by the new technologies, markets and programmes of the Fourth Industrial Revolution and the Great Reset of Western capitalism it has enabled. It’s not impossible that reception of UBI will eventually be made conditional on accepting a Radio Frequency Identification (RFID) chip implanted under the skin that would not only allow us to receive and make payments, but also for the state to track our movements and monitor and limit those payments. One might soberly reflect that no-one is going to give us ‘free money’ unless they have absolute control over how we spend it.

A system of Social Credit modelled on that currently employed in the People’s Republic of China, in which both citizens and businesses are given a credit rating based on their compliance not only with the laws but also with the behavioural norms of the state. Among other means suggested by the International Monetary Fund in August 2020, this rating will be established through access to our personal online browsing, search and purchase history, and the compliance of our businesses with criteria of production, consumption, sustainability, employment rights, trade partners, etc.

Facial Recognition technology, which the police in the UK have already been using for some time to stop and search members of the public without cause in order to build up a database of the population, and which will be used in conjunction with Digital ID to identify citizens not compliant with the norms and regulations of the biosecurity state. As we have had demonstrated to us over the past three years, these are not being made by our elected national governments but rather by unelected and unaccountable international technocracies overseeing global finance, expenditure, consumption, energy, health, agriculture, animal husbandry, education and, as we are seeing in the Ukraine, war.

Smart Cities, in which our freedom of movement, assembly, association, access, business, consumption, ownership, privacy, expression and thought will be monitored, analysed and controlled by the Internet of Things by which we are increasingly surrounded. Since at least 2018, the Trilateral Commission has promoted the use of Artificial Intelligence technology to analyse, monitor and shape our behaviour.

This is currently being implemented in the UK by local authorities enforcing the restrictions of so-called 15-minute cities, an invention of the World Economic Forum that violates our Freedom of Movement under Protocol No. 4, Article 2 of the European Convention on Human Rights. These restrictions on what initially is stipulated as the number of times we are allowed to leave our designated limits in a car will be monitored by a panopticon of surveillance equipment, with punishments starting at fines and extending, undoubtedly, to electric cars being ‘switched off’ and other punitive measures already in use in China’s system of social credit, such as being refused the use of even public transport.

Those who justify such restrictions ‘because it’s in a car’ are the same who justified lockdown, masks and mandatory gene therapy, and equally blind to where it will lead. Once you accept that human rights are contingent on what the state declares is the common good, you’re on the road to fascism. And if we think this only applies to cars and is being implemented to ‘save the planet’, London Underground is implementing ‘Smart Stations’ using AI technology to monitor, record, analyse and learn from our every movement and action. It is a short and rapid step from stopping someone from leaving a jurisdiction in a car, bus or train to stopping them leaving—or entering—without other technologies, like Digital Identity and even more intrusive biotechnology.

As an example of which, the Internet of Bodies by which we are connected to this system of surveillance and control includes, so far, pharmaceutical products carrying a microchip registering when they are and are not ingested to ensure ‘compliance’; a quantum dot dye delivered with gene therapy that stores information about the injected person’s medical history and biosecurity status; a microprocessor storing encrypted payment data implanted under the skin of our hand to allow contactless payments; a smartphone app that tracks our individual carbon footprint in order to monitor and control what and how much we consume; and a microchip implanted in our brain to augment the reality of the conditions to which they want to restrict us.

You’ve probably heard these being dismissed as ‘right-wing conspiracy theories’ in the mouths of snorters in Parliament and the propagandists for compliance in our media. But the microchipped tablet was announced by Albert Bourla, the CEO of Pfizer, at the World Economic Forum in January 2018; the quantum dot dye vaccine by researchers funded by the Bill & Melinda Gates Foundation at the Massachusetts Institute of Technology in December 2019; the skin implants by Walletmore, a Polish-British startup company, in October 2021; the carbon footprint tracker by the President of the Alibaba Group at the World Economic Forum’s annual meeting in May 2022; and the brain implant by the Vice-President of Research and Design for IMEC, the nanoelectronics and digital technology company, on the website of the World Economic Forum in August 2022. Indeed, when it comes to the technologies of our enslavement, our conspiracy theories have fallen well short of the digital, virtual and augmented reality being prepared for us by the enemies of humanity.

Our listing of Great Reset programmes continues with the Pandemic Prevention, Preparedness and Response Treaty, launched by the World Health Organization in December 2021 and adopted by the European Council in March 2022. Under this treaty, the 194 member states of the World Health Organization will be legally bound to implement restrictions on human rights and freedoms, such as mandatory face masks, lockdowns, compulsory gene therapy, Digital Identity and worse, on the judgement of an international health technocracy that is funded by and subject to lobbying by the most powerful nations and international companies in the world, and in particular of its largest private funder, the Bill and Melinda Gates Foundation.

The basis of this agreement is Article 19 of the Constitution of the World Health Organization, which states that the General Assembly can adopt agreements that, if passed by a two-thirds majority, are constitutionally binding on all member states. Under this agreement, nation states, including the UK and the 193 other members of the WHO, will in principle concede their sovereignty to decide which restrictions the elected executive and legislature will impose on their populations.

Crucially, once written into a legally-binding treaty, the efficacy or logic of these biosecurity ‘measures’ will no longer be open even to what little debate we’ve had in this country. Instead, the WHO will effectively become a global form of the UK’s Scientific Advisory Group for Emergencies (SAGE), a politically-appointed technocracy to which the governments of nation states must defer if they wish to retain their status in the Global Biosecurity State, and which serves to depict undemocratic and unaccountable forms of governance as technical responses to new crises.

Then there are the Sustainable Development Goals, which were adopted by the United Nations in 2015 under the rubric of Agenda 2030. Behind their humanitarian objectives, these seventeen edicts allocate the flow of global capital, investment and other preferential treatment to governments and corporations according to their compliance with Environmental, Social and Governance criteria. Despite their UN branding, these are formulated and imposed by the wealthiest and most powerful international corporate asset managers like BlackRock, the Vanguard Group and State Street Global Advisor.

Far from saving the planet from exploitation by multinational corporations, the Sustainable Development Goals are designed to increase the monopoly of wealthy Western economies and international companies able to meet their criteria over poorer countries, and to create the framework for purchasing their UN-assigned quota of emissions in carbon credits. On the same justification, developing countries are loaded with debt by financial organisations like the World Bank and the International Monetary Fund in order to meet these goals, and those unable to meet repayments through increased taxation and spending cuts to their already impoverished populations will be invited to hand over their land and natural resources to their debtors.

And finally, there is Central Bank Digital Currency, which employs blockchain technology to log every transaction we ever make and is programmable, as we have seen, with restrictions and limits on expenditure contingent on, for example, our biosecurity status, carbon footprint and social compliance.

Could it, for example, be used to switch off access to digital money for those who violate the limits of 15-minute cities? Or of those who fail to meet the biosecurity state’s definition of ‘fully vaccinated’? Or of those who fail to upgrade their car to an electric vehicle, neglect to recycle their rubbish, eat more than their allotted quota of meat and dairy products, or leave their heating on beyond the allotted times? Or of those the state describes as a threat to the ‘common good’ for daring to criticise the government, or indeed the central banks? When our salaries and our savings are in CBDC, it will no longer be necessary to evoke emergency powers, as the Government of Justin Trudeau did in February 2022, to freeze the bank accounts of the non-compliant without a court order.

In effect, CBDC will become a form of geo-fencing, but instead of receiving an electric shock in our ear for transgressing beyond the limits of our 15-minute grazing range, we will have our access to the necessities of life removed, including work, healthcare, energy or food from animals or crops that haven’t been genetically modified.

The question I am trying to formulate is whether—given the contexts in which it will be implemented and the demonstrated willingness of the governments of the West to lockdown, spy on, control the movements of and punish their citizens for the ‘common good’—CBDC is likely to be so programmed. It clearly can be. These contexts, I would suggest, make it more than likely that it will be, and, indeed, that this programming is the primary but undeclared purpose of Central Bank Digital Currency.

3. Towards Absolute Control

As I mentioned above, the Bank of England has said that it is working with the Bank for International Settlements, the central bank for its membership of 63 central banks that account for about 95 per cent of world GDP, and which include the Bank of England, the European Central Bank, the Bank of Japan, the People’s Bank of China and the US Federal Reserve System. Its General Manager, Agustín Carstens, the primary advocate for the adoption of CBDC by its members, in December 2020 made this by now famous statement about the ‘general use’ of Central Bank Digital Currency:

We tend to establish equivalence with cash, and there is a huge difference there. With cash, we don’t know who is using a $100 bill today. A key difference with CBDC is that central banks will have absolute control over the rules and regulations that will determine the use of that expression of central bank liability. And also, we will have the technology to enforce that. Those two issues are extremely important, and that makes a huge difference with respect to what cash is.

What appears certain is that CBDC will allow central banks to act like commercial banks in providing loans to both private- and public-sector lenders. This is what happened following the second Global Financial Crisis in twelve years that started with the spike in interest rates in the repurchase agreement market in September 2019, three months before anyone had heard of Covid–19, and six months before lockdown was imposed across Western economies.

On the suggestion of BlackRock, the largest asset manager in the world with $10 trillion in assets under management, the US Federal Reserve injected hundreds of billions of dollars into the financial system, effectively providing zero-interest loans to JP Morgan, Goldman Sachs, Barclays, Deutsche Bank, the Bank of America and other favoured commercial banks. By July 2020, the cumulative value of these loans was $11.23 trillion.

As a result of this vast quantitative easing programme, which was adopted around the world on the justification of sustaining national economies under lockdown, by April 2022 the total assets of the US Federal Reserve (which had reached $8.9 trillion), the European Central Bank ($9.6 trillion), the Bank of Japan ($6.2 trillion) and the People’s Bank of China ($6.3 trillion) had risen to $31 trillion, an extraordinary and unprecedented increase from $19 trillion in September 2019. And although this has fallen to $28.5 trillion this month, across the globe over $41.4 trillion in assets, nearly half the world’s GDP, are now held by central banks.

With this increase in assets comes a corresponding increase in the liabilities over whose rules and regulations Agustín Carstens wants ‘absolute control’. Liability, or what a bank owes to others, includes the total amount of currency in circulation, the reserves in commercial banks, mortgage-backed securities and equity capital, and with it the risks to the real and financial sectors of the economy.

We should remember that, when we think we are depositing our money into a bank, we are, under law, doing nothing of the sort. As explained by Richard Werner, the economist who invented the monetary policy of quantitative easing for the Bank of Japan in 1995, what we do when we think we deposit our money in a bank is make a loan to the bank, which borrows from the public. And equally, when we think we take out a loan from a bank, in reality the bank purchases a security—which is to say, a promissory note—which is issued by us to the bank. But no money is transferred to our account.

What we call a deposit is merely a record the bank makes of its debt to the public. And what we think we are receiving as money from a loan is merely the bank’s record of what it owes us. Banks, despite their protestations to the contrary, are not intermediaries between depositors and lenders; they are magicians that magic money into existence with a sleight of hand. Having purchased our promissory note, they record what is an accounts payable liability arising from the loan contract as a customer ‘deposit’; but no money has been deposited. When banks lend, they create money out of nothing by inventing fictitious claims on themselves.

As long as bank credit—which is to say, the creation of money—is for investment and loans for new goods and services that add value to the economy, it creates stable economic growth without inflation. However, when money is created to increase consumption, inflation rises, which is what is happening across the world as the vast sums of magic money printed to shore up the collapsing financial sector have entered into the real economy.

Worse still, when money is created for financial transactions—which make up over 70 per cent of all lending in the UK—banks, rather than adding value to the economy, create new purchasing power over existing assets, whose prices are thereby pushed up: land prices, housing prices, as we’ve seen over the past two decades, and as we’re experiencing now, energy prices—creating greater and greater inequality.

One of the purposes of CBDC is to ensure that small, independent banks, with the power to make money, don’t start lending money to small and medium-sized businesses to create new goods and services, thereby reducing inequality and increasing our independence from both the state for investment and the financial sector for credit.

When Central Bank Digital Currency has been implemented and doesn’t ‘exist alongside’ cash (as the Bank of England assures us) but has instead replaced it (as seems far more likely), what we think of now as ‘our’ money will instead be, as Agustín Carstens very precisely phrased it, an ‘expression’ of Central Bank liability.

What this means—what it could mean, what it appears likely to mean, what the wider contexts in which CBDC is being implemented overwhelmingly indicates that it does mean—is that if the central bank doesn’t approve of how we are expressing its liability, it will have what Carstens boasted are the ‘rules’, the ‘regulations’ and the ‘technology’ to limit and control where, when and on what we can spend their money, up to an including the point of us having none to spend.

As the Bank of England and HM Treasury have specified, the private Payment Interface Provider—which is to say, the most powerful commercial banks and information technology companies—will have the technology to programme conditions into CBDC that will activate a locking mechanism when they are not met or violated. And since these private providers are operating under the Environmental, Social and corporate Governance (ESG) criteria imposed by BlackRock, Vanguard, State Street Global Advisors and other corporate asset managers in furtherance of the UN’s Sustainable Development Goals and the signed commitment of the governments of the West to Agenda 2030, they will be obliged—doubtless with a show of protest—to programme CBDC with the limits and requirements on expenditure and consumption that meet these goals and this agenda.

The key point is, this will no longer be our money but instead an expression of Central Bank liability. The Bank of England is liable for how, when and on what we spend its digital currency, and it is the central banks and other stakeholders that compose the new global technocracy that will determine the rules and regulations by which we spend it. Programmable CBDC is the technology.

Since its founding in 1694, the Bank of England has made it clear that the pound sterling is a promissory note, with the terms written on the paper notes we call cash. ‘I promise to pay the bearer on demand the sum of X pounds’, declares the note, signed by the Chief Cashier ‘for the Governor and Company of the Bank of England’. When cash has been withdrawn as a form of currency and there is no longer anything for us to ‘bear’ in our wallets (and one day, perhaps, even in our private bank accounts), that promise to pay will lie within the purview and liability of the central bank, and what we now call money will be reduced to the expression of its largesse. That, I believe, is what Agustín Carstens means by ‘absolute control’.

Even for the overwhelming bulk of the British population that does exactly as it is told—including injecting experimental gene therapies into its own arms and those of its children, remaining within the boundaries of its 15-minute cities, consuming its allotted share of insects, and taking, without question or complaint, what it is given—CBDC will keep it poor and compliant. ‘You’ll own nothing. And you’ll be happy’, as the World Economic Forum has been telling us for many years now, or we will, ultimately, be deprived of the necessities of living. Central Bank Digital Currency is part of the infrastructure for a tokenised economy: currency not as a means of exchange but as reward for compliance.

This is what Tom Mutton intimated when he said that the Digital Pound ‘can support wider public policy objectives’ and prevent ‘activity which is seen to be socially harmful’. Under these terms, CBDC will be an automated form of governance enforced outside of any legislative or juridical mediation. Comply or starve. This is a system of totalitarian control, the likes of which the world has never seen before, and it is being implemented now.

And once implemented, short of a revolutionary overthrow of the Global Biosecurity State, it will be very, very difficult to reverse. Indeed, in the written evidence submitted to the UK Parliament in September 2022, the Digital Pound Foundation, whose board members have numerous links individually or through partner companies to the World Economic Forum and which is partnered with Ripple, the blockchain-based digital payment company, wrote:

The introduction of new forms of digital money—whether public or private in form—is irreversible.

I, for one, believe them, as does Richard Werner, who understands CBDC far better than I ever will, and who is unequivocal about its purpose. At a conference held by the Monetary Institute in Switzerland back in February 2018, he described the bid for Central Bank Digital Currency to achieve ‘total control over all economic transactions’ as ‘the greatest concentration of central banking power in history’, the aim of which is ‘an Orwellian dystopia of total control over people and the end of any freedoms’.

Was he right? Well, in Nigeria, the only large country to have implemented CBDC, the results have been disastrous. As Nick Corbishley, who has been following its implementation closely, has reported: out of a population of nearly 220 million people, only 905,000, or 0.4 per cent, have downloaded a digital wallet, and a mere 282,600 accounts are active. In response, the government has issued repeatedly deferred deadlines for the withdrawal of cash from circulation.

As a result, some 80 per cent of the $7.2 billion previously held in private hands has been deposited with financial institutions, and a limit of around $225.00 per week has been imposed on cash withdrawals for individuals and five times that for businesses, leaving the population with an acute shortage of money and businesses unable to trade. Further reductions have been threatened. Unlike the Bank of England, the Central Bank of Nigeria has been open in its declarations that the motivation for these monetary restrictions is the drive towards a ‘cashless economy’.

I’ll end with a question. In February of this year, at the World Government Summit held in Dubai, Klaus Schwab, the Founder and Executive Chairman of the World Economic Forum—which for decades has worked to replace the sovereignty of nation states and governance by democratically elected representatives with the rule of an unelected technocracy in a global political economy he calls ‘stakeholder capitalism’—declared that those who master the new technologies of the Fourth Industrial Revolution will be ‘the masters of the world’.

So my question to you is this. What do you think this new Master Race founding another Thousand-Year Reich will do with Central Bank Digital Currency?