As a small boy my earliest memories of banking are of going into the huge (to me) main banking hall of the Airdrie Savings Bank with my mother and a large glass jar, full of threepenny bits. This was banking Airdrie style, with real savings and a bit of grandeur to the experience. The double-height neo-classical banking hall, the atmosphere of hushed concentration from the staff, the massive portraits on the wall, one of a gallant chap in red British Army dress uniform and wearing a fine feathered military hat, made quite an impression on me. Then, of course, there were no bandit screens between the staff and the customers. One felt like a welcomed investor. I could have been in London or New York, investing millions, and not have been treated any better than I was as a small boy with a jar of oddly shaped brass coins.

Such was banking in the late 1960’s. Even then the Airdrie Savings bank (ASB) was an outlier. The only independent savings bank left in the United Kingdom; the only one to refuse to be swallowed up into larger organisations. But it worked well, in those days, where the pound was tied to the dollar and the dollar was tied to gold and gold was real money that could neither be printed nor counterfeited.

Looking back with adult eyes, the sequence of causes and effects that was to eventually destroy this organisation was already in place. The news in the evenings was full of helicopters and gunfire, for the war in Vietnam was in full flood. Wars, we must remember, are expensive things and are paid for not only in blood but also by devaluing currencies and silently robbing populations. Bombs were needed and, so, also, were dollars. The dollars were duly printed and the gold drained away from the US hoard. First a trickle and then a deluge. In 1971, President Richard Nixon went on TV and told the American people and the world about the evil speculators and the need to protect the financial security of America. He said he was temporarily suspending convertibility of the dollar into gold. What he really said was the US was bust and was defaulting on its debt. The last tether to reality was severed in world financial markets, the last restraint gone. For the Airdrie Savings Bank, the die was cast but it would be a generation before events worked themselves out.

Unrestrained fiat currency manipulation saw inflation in the 1970s, speculation in the 1980s and a transition to the "PhD standard" - control by wise economic sages such as Alan Greenspan—in the 1990’s. We were told this was an end to boom and bust. We were told the central bankers now had the wisdom, the power and the data to fine tune the world financial system for peak performance and peak communal wellbeing. Banking had become sexy, it had become politics, or perhaps it had become faith. It was all a long way from Airdrie and from thrift. The effects were visible first in the real economy, where the good productive jobs ebbed away from the town of Airdrie and the independent spirit that had built and maintained the bank was slowly eroded. But the bank continued almost as before. Yet now there were bandit screens between the tellers and the public.

And now we come to 2008. The 11th September (interesting date) to be precise. The whole banking system stood on the brink, hours from a complete collapse. There would be riots, blood in the streets, martial law, starvation and panic—unless the government, via its ability to extract wealth by taxation, bailed out the banks. And bail they did.

For a while “banker” was term of abuse as people realised how much was paid, and how much ordinary people were suffering. Some, with an eye for cause and effect traced the problem from the PhD standard in monetary regulation to the wild greed of the big banks and the “Greenspan Put”. Some looked for an alternative model. Some even looked to Airdrie. In 2010 new investment came in to encourage expansion. This was directly and explicitly a reaction to the 2008 banking crisis.

A group of Scotland’s leading businessmen have come together to support the expansion of Airdrie Savings Bank outside of its Lanarkshire homeland.

The list includes Brian Souter, Ewan Brown, Alastair Salvesen, Sir Tom Farmer, Ann Gloag, Sir Angus Grossart, Sir David Murray and DC Thomson & Co Ltd. They plan to create at least one, and possibly two new branches over the next 18 months, [this] comes as the bank celebrates its 175th birthday.

In addition, Airdrie Savings Bank is looking at developing an account-opening network in Scottish towns and cities where there is a proven demand for its services. The bank has also been investing in internet banking as a platform to support expansion.

Bob Boyle, president of Airdrie Savings Bank said: “The trustees are delighted that so many prominent Scottish business figures have come forward to back our ambitions to expand. Several are supporting us through a combination of deposits and borrowings.

“Airdrie Savings Bank, as you would expect, is approaching expansion with caution. We will dip our toe in the water by opening one branch at a time to prove the sustainability of growth before considering more ambitious plans.”

Brian Souter said “Airdrie Savings Bank represents what Scottish banks once stood for – security of funds, a focus on savings and outstanding personal service.

“We aim to bring this traditional blend to the people of Scotland by supporting the bank’s development as we believe the mutual principle is fundamental to the integrity of the bank.

“We are doing this because so many Scots are dismayed at what has happened within the banking sector.”

But from the optimism of 2010, to the closure of 2017 what has happened? It was not a case of over expansion. The bank has no problem with inadequate reserves (theirs are over three times greater than required by the government regulator). Rather it is a story of slow strangulation by the very regulations that politicians claim will prevent risky behaviour by banks and will encourage the wise stewardship of resources that had been the modus operandi of the ASB since 1835. In other words the cure was the killer.

Chairman Jeremy Brettell said: "Whilst we are financially strong, a comprehensive strategic review of all future options concluded that we will not have—as a very small bank—the resources in the years ahead to provide the products and services our customers need in this increasingly digital world.

"The decision to implement a phased end of business activities is totally consistent with the overriding responsibility of our Board of Trustees to protect the best interests of our customers, both now and in the future."

Chief executive Rod Ashley said: “In taking this difficult decision, the trustees have taken full account of the bank’s proud history.

“However, we are in absolutely no doubt that acting now from a position of financial strength is both prudent and responsible, and in the best future interests of our customers.”

Mr Ashley cited a “shrinking customer base” and “declining footfall” as contributing to the closure.

He said: “Sad as the course of action outlined today is – in terms of our history and heritage – we are in absolutely no doubt it is in the best future interests of our customers.”

The hidden effects of regulation which prevent competition with established interests, stop innovation dead in its tracks and disproportionately burden smaller firms are well known in (Austrian) economic circles, but politicians still succeed in selling this to the public as a restraint upon large corporations. It is in truth a restraint upon the free market and the little guy and a subsidy to the large corporations.

Consider the specific case of the Government’s banking deposit guarantee. This work of fiction claims the government, in the event of a bank collapse, will reimburse savers for the first £85,000 (Euro 100,000) lost in any collapse. For the masses, who believe the plain written meaning of the words, this means that more conservative careful organisations are no safer than the risky ones – for the government guarantees that all banks, and all depositors shall be equal. The natural free market advantage which would normally accrue to risk averse and wisely run organisations is wiped out to all but those few investors who do not believe that tiny reserves in government hands can guarantee a massive financial industry.

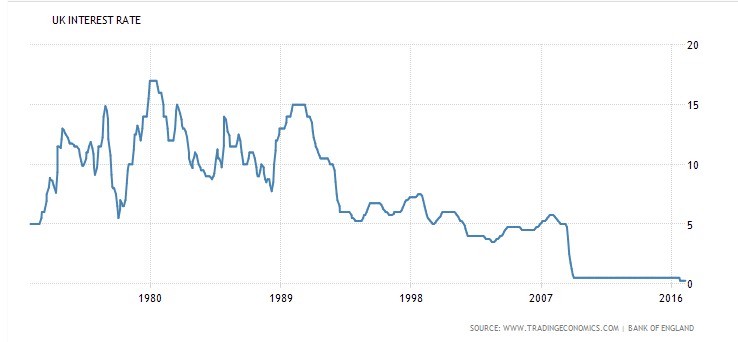

Furthermore, for the ASB, it is not merely regulation that is to blame, for the income of the bank was also hit. That income came from three main sources: deposits held in other (larger) banks, loans to the public secured against property and the purchase of UK government debt.

All have been hit by the unprecedented zero Interest rate policy (ZIRP).

This has maintained an unrelenting squeeze on the bank, not sufficient to create losses for the overheads are low by virtue of ASB’s uber-thrifty corporate structure:

No shareholders

The Bank has no shareholders. It does not need to pay dividends and any surpluses are available for reinvestment for the benefit of customers. The Bank is governed by a Board made up of Trustees and Executive Managers. The Trustees give of their time without remuneration and have no financial interest in the Bank's progress. This form of corporate governance is another of the Bank's unique qualities.(ASB Website)

But rather the reduction in interest rates has hit the ASBs income and forced it to likewise lower the interest it pays to savers to almost nothing. Without an incentive to save or at any rate to save via an institution such as a bank, why would people cross the threshold? Keeping the money in cash, in a Paypal account, or anywhere else where it is safe but yields no interest, is just as good as a bank in the world of ZIRP. Worse, saving at all becomes less attractive. Rather debt, being subsidised, grows and families find themselves evermore in its unforgiving grip.

In summary, all incentives to thrift, to the careful management of scarce resources, are obliterated in the modern world of fiat money, PhD economists and zero percent interest rates. They are replaced by a burdensome regulatory environment, and by a financial system where money is free for bankers and almost free for the public. As a result, thrift dies, replaced by theft from savers and subsidy to speculators. Like the service I once received as a small boy in the Airdrie Savings Bank, I shall miss it.